While there are many challenges that come with building a house, it probably can't get much worse than hearing your builder has gone bankrupt and that work to your home has stopped, effective immediately.

The so-called 'profitless building boom', triggered by the COVID pandemic, is still playing out in the Australia construction sector, seeing thousands of home builders collapse with more still to come, according to industry watchers. If you're signing a contract to build your own home, it's important to know what to do if it happens to you.

Why are builders going bankrupt?

Australia's construction industry is still feeling the effects of the COVID-era 'perfect storm' that has sent thousands of builders, and associated trades, to the wall.

Amid an economy crippled by lockdowns, the federal government's HomeBuilder grant program was launched in June 2020 as part of wider stimulus package. Government handouts under the scheme generated record new home sales at the same time mortgage rates were at record lows.

As demand climbed, builders took on more and more standard fixed-priced contracts only to be hit by global production and supply chain issues, driving drastic shortages of building materials and sending prices skyrocketing.

On top of that, with migration halted during the pandemic, there were not enough workers to build the homes promised, forcing labour costs up at the same time. Many builders could only absorb the mounting cost pressures for so long.

In 2023, a record 2,349 construction firms were declared insolvent, according to data from the corporate regulator ASIC. In 2024 so far, on average more than 200 building and construction companies are still going under every month. Some industry commentators have labelled the period a 'property cyclone'.

Why are builders still going bust if prices are stabilising?

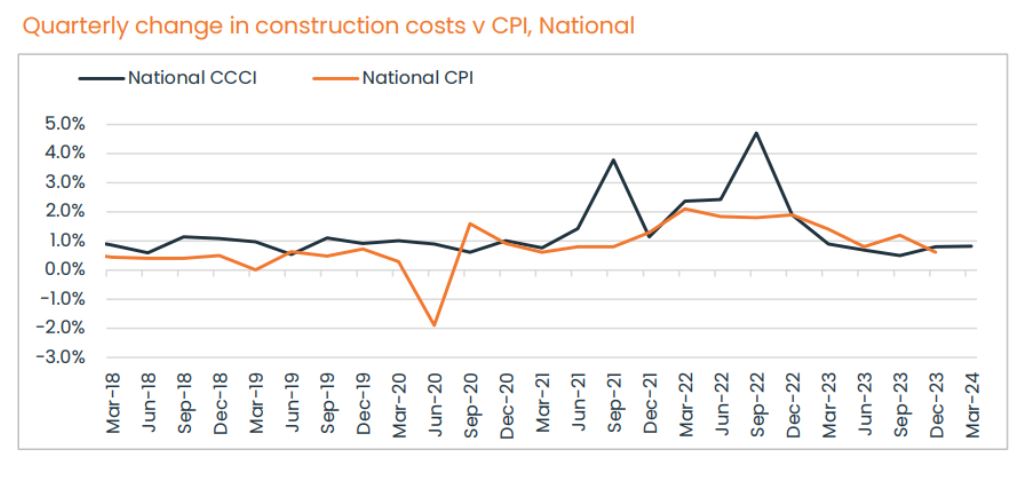

According to data from the ABS, residential building material price hikes have slowed considerably from their peak. The time of writing, the latest ABS figures from March 2024, show home construction costs were up 1.3% on an annual basis. That's well down from the height of 17.3% in July 2022.

Annual data from June 2022 saw prices for reinforcing steel jump 42.2%, timber 40.7%, and steel beams more than 37% over the previous 12 months. Over the same period, the labour cost of bricklayers increased 16.4% while carpenters and painters were both charging over 12% more.

Yet, 2023 saw construction costs ease from their record highs, as illustrated below:

Source: CoreLogic

According to CoreLogic's Cordell Construction Cost Index, the cost of building a typical new dwelling recorded a modest 0.8% rise in the first quarter of 2024, remaining stable with the increase seen in the last quarter of 2023.

But CoreLogic economist Kaytlin Ezzy said the huge backlog of unfinished homes continues to put significant pressure on builders' profit margins.

"The construction pipeline remains bloated with ABS building activity data showing around 255,000 dwellings approved but not yet completed," she said.

For some builders bound by historic fixed-price contracts, many of these incomplete homes will cost them more to finish than they will make out of them. As well, builders continue to be hit by labour shortages and tighter access to capital in keeping their businesses solvent.

How do you know when a builder has gone insolvent?

There may be certain tell-tale signs your builder has gone insolvent.

Lawyer Richard Hutchings of Cornwalls Law specialises in the building and construction sector. He advises if you see symptoms of a project that's badly behind or being mismanaged, you should immediately check the ASIC register to find out if the company is deregistered or insolvent.

"Often, owners find out the builder has ceased operations when they have not been seen on site for a period of time and there's a disconnected phone line," he told Savings.com.au.

"There is often a correlation between jobs that are badly delayed and badly managed, and then the builder becoming insolvent."

Other signs your builder may be in financial difficulty include:

-

poor communication, both with you and suppliers

-

late with payments to suppliers, contractors, and/or employees

-

legal disputes with suppliers and contractors

-

defective work or using poor-quality materials may be a sign a builder is cutting corners to save costs

Mandatory builders' insurance

Before your project even begins, it's mandatory (in most states anyway) that your builder takes out insurance designed to cover you, the client, in the event they go bust, disappear, pass away, or, in some states, have their license suspended. (As at May 2024, the Tasmanian government is working to reintroduce a state-mandated insurance scheme while the Northern Territory provides cover from a not-for-profit fidelity fund.)

The insurance goes by different names depending on what state or territory you're in, including builders warranty insurance, home warranty insurance, or home building compensation cover, to name but a few. In all cases, the insurance is purchased by the builder, although the premiums will be passed onto you in some form.

"The builders warranty insurance is there to try and give you a chance to cover defective works, the extra over costs for incomplete works, and otherwise give you a bit of support in the event of the builder falling over," Mr Hutchings said.

The rules and cover differ between jurisdictions. Where mandatory insurance applies, your builder should provide you with a copy of the insurance certificate before your job starts. If you don't receive it, you need to ask questions and make sure you get it before the job begins. The general advice is don't pay your deposit until you receive it.

"It's not uncommon for builders that are in a difficult financial position to not pay for that insurance to try and save money," he said.

"Owners should be watching out for this and ensuring they receive certificates of insurance as required under the contract and checking that they are correct or seeking legal advice if they're unsure."

Here are the current insurance schemes for the states and territories and where to find further information:

|

State |

Insurance scheme |

Legal status |

Further information |

|---|---|---|---|

|

New South Wales |

Home Building Compensation Fund |

Mandatory for work valued over $20,000 |

https://www.service.nsw.gov.au/guide/home-building-compensation-cover |

|

Victoria |

Domestic Building Insurance |

Mandatory for work valued over $16,000 |

|

|

Queensland |

Home Warranty Insurance |

Mandatory for work valued over $3,300 |

|

|

Western Australia |

Home Indemnity Insurance |

Mandatory for work valued over $20,000 |

|

|

South Australia |

Building Indemnity Insurance |

Mandatory for work valued over $12,000 |

|

|

Australian Capital Territory |

Residential Building Warranty Insurance |

Mandatory for work valued over $12,000 |

|

|

Tasmania |

Residential Building Warranty Insurance (proposed Bill) |

Voluntary only until mandatory scheme is set up. |

|

|

Northern Territory |

Master Builders Fidelity Fund annual cover for builders |

Certificates must be issued for residential building work and renovations over $12,000 |

It's also worth noting mandatory builders' insurance does not cover all eventualities including worksite accidents that cause property damage, or the theft of building materials or equipment left at the site (in most states).

State and territory requirements

New South Wales

In New South Wales, builders are required to take out home building compensation (HBC) cover (formerly known as home warranty insurance) for each home building project over $20,000.

The total limit (including non-completion of building work, defective building work, and any other costs covered by the policy) is $340,000 per dwelling, with a sub-limit for incomplete work of 20% of the contract price.

Insurance under the HBCF allows consumers to make a claim for a loss caused by the contractor's defective or incomplete work in the event of the contractor's insolvency, death, or disappearance. Claims must be made within 12 months of the date the work stopped or failed to start. Major defects are claimable for a period of up to six years of the completion of the work.

The scheme is underwritten by the New South Wales insurance corporation icare. Its website details how to make a claim.

Victoria

Victorian builders are required to take out domestic building insurance (DBI), also known as builders warranty insurance, for work valued at more than $16,000.

If your builder goes bust, you can make a claim on the policy by notifying the builder's insurer within 180 days of becoming aware of the builder's insolvency.

Claims are limited to a maximum $300,000 to fix structural works for a period up to six years, with incomplete works capped at 20% of the total contract price. Typically, most builders in Victoria are insured by the Victorian Managed Insurance Authority (VMIA).

Queensland

Residential building work in Queensland valued at more than $3,300 must have insurance through the Queensland Home Warranty Scheme (QHWS), administered by the Queensland Building and Construction Commission (QBCC).

If your builder has not completed the contracted works, or if you have paid a deposit and building work has not started, you may be able to make a claim.

It's important to note that to lodge a non-completion claim, you must have signed a fixed-price contract for the home. The maximum claim you can make is $200,000. However, this increases to $300,000 if optional additional cover has been taken out.

If no work has started, QBBC will refund the deposit already paid or if work has begun, it will stump up for the difference between the funds you still hold under the contract (or should hold) and the cost of completing the work. Claims must be lodged within three months from the date the contract ends although time limits vary for different claims depending on the type.

In Queensland, claims can also be made for vandalism and theft, but this is part of the $200,000 cap for non-completion and comes with an excess. The QBCC website contains more information about making claims.

Western Australia

Western Australian builders must take out home indemnity insurance (HII) for all residential projects valued at more than $20,000, regardless of the type of contract.

HII covers lost deposits up to $40,000 and completion costs up to a maximum of $200,000. Claims must be made up to six years from practical completion with a $500 excess. As at May 2024, cover is provided by QBE Insurance, as approved by the Western Australian Minister for Commerce.

South Australia

In South Australia, builders must take out building indemnity insurance (BII) for any residential work that requires development approval and has a value of $12,000 or more. BII protects the homeowner against financial losses in the event that the builder dies, disappears, or becomes insolvent before the completion of the work.

The maximum amount claimable is $150,000 if the policy was issued on or after 1 July 2017. For those policies issued before then, you can only claim up to $80,000. Claims can usually be made up to five years from the date the building work was completed.

To make a claim, you must contact the relevant insurer to get the process started. The South Australian government provides details of BII insurance providers according to the time period the insurance was taken out.

Australian Capital Territory

Builders must apply for either:

-

residential building warranty insurance

-

or a fidelity certificate issued by the trustees of an approved fidelity fund scheme (currently the Master Builders Fidelity Fund)

for work valued over $12,000. It covers homeowners for loss of deposit and incomplete/defective building work in the case their builder dies, disappears, or becomes insolvent.

In the ACT, the insurance policy provides for a maximum cover of $85,000 and up to $10,000 for loss of deposit, the lowest of all the states and territories. The relevant insurer must be informed within 90 days for insolvency issues with a period of up to five years for defective building claims.

Northern Territory

In the Northern Territory, residential building cover is issued in the form of a fidelity fund certificate from the Master Builders Association Northern Territory. It covers the homeowner for costs associated with transitioning to a new builder in the case their current builder becomes bankrupt.

It also covers fixing structural defects for six years after completion or non-structural defects in the first year after completion. The maximum claimable is $200,000 with cover capped at 20% of the contract price. To lodge a claim, contact Fidelity Fund NT directly.

Tasmania

Tasmania scrapped mandatory builders' insurance in 2008 in a bid to reduce the cost of housing in the state. It has since moved to reintroduce an insurance scheme through legislation in the state's parliament. As at May 2024, the scheme was still being established.

Problems with builders' insurance

In most states, builders' insurance, under its various guises, is known as insurance of 'last resort', that is, it will provide some cover if all other avenues of recovery or rectification are exhausted. It is generally triggered if your builder becomes insolvent, goes missing, dies, or loses their licence.

It doesn't always apply if building work is simply shoddy (unless there's a court order in some states) or if your builder refuses to make good. That can require going to consumer affairs tribunals in some jurisdictions which can be a lengthy and costly process. But builders' insurance is a safety net and better than no recourse at all. Make sure you take note of claims periods and act promptly as soon as you become aware of any issues.

First steps when you discover your builder has gone bust

-

Stop all payments immediately and contact your bank to stop any in progress from going through. You can also decline to pay any outstanding or issued progress payments. This will ensure your losses from the incomplete works are minimised.

-

If you have taken out a loan to fund your building project, contact your lender and let them know. They can help you understand your obligations and lenders' rights in the event of builder bankruptcy. It's also worth checking whether you have any loan protection insurance covering such situations.

-

Contact the relevant insurer to get some general advice and understand your position under the cover you have.

-

If your builder has gone through the formal steps of declaring insolvency, an insolvency practitioner will be appointed as an administrator of the builder's financial affairs. They may contact you, but you are within your rights to contact them to help you understand what is happening with the builder's assets and whether there are any funds that may be available for the completion of your home. You may choose to engage a lawyer to communicate on your behalf.

-

Seek legal advice. Mr Hutchings strongly recommends seeking legal advice prior to making a claim on any building insurance policy (or policies) you have or terminating your existing building contract.

How lawyers can help with the process

Lawyers can give advice on individual building contracts and specific circumstances. All contracts are different and your contract may contain its own provisions on what constitutes insolvency and your rights if it occurs.

As well, Mr Hutchings warns against terminating your existing contract without legal advice, even if you are keen to move on and find another builder to complete your home. Believe it or not, a builder becoming insolvent is not sufficient grounds for contract termination on its own and a lawyer can advise on what grounds and notice periods are required in your particular circumstances. Lawyers can also help prepare cases for claims covering defective or incomplete works.

"With the help of a lawyer, you can also obtain a defects report which makes it very clear what the defective works are [structural and non-structural], how much it will cost to fix them, and how to maximise your recovery [claim] under any relevant insurance policy," Mr Hutchings said.

You may also want to engage a lawyer to assist in contract negotiations with a new builder who is appointed to take over the construction. These contracts can be more complex given work may already be underway and there will likely be liability issues for the work already done.

Be sure to get some idea of the cost involved in getting legal advice upfront. It can add considerably to the expenses you will likely already be facing. Legal advice can be invaluable in some circumstances but may not see you receive more than you're entitled to under existing mandatory insurance or fidelity fund schemes.

Savings.com.au's two cents

There's no crystal ball to predict which builder will go bust. Even some of Australia's major construction companies including Porter Davis Homes Group (at the time ranked the country's 13th largest builder), Condev, Clough Group, and Probuild, have gone under in recent years.

Although there's not much you can do to stop a builder from going insolvent, there are some things you can do to mitigate the damage. The big one is to make sure your builder has taken out builders' insurance, as mandated by law in most states and territories, and that you have the certificate for it before work begins. Alas, it may not cover you for all your extra expenses if your builder collapses, but it can provide some recompense.

If the worst happens and your builder becomes insolvent, read the contract you have to see what it says about such circumstances. It may provide some details for you. There are also comprehensive guides on what to do next according to what state or territory you are in, with official links supplied in this article.

Be aware of what avenues are open to you, keep meticulous records, submit your claims promptly, and seek legal advice if it all becomes too complex or overwhelming. Unfortunately, there is little free legal advice out there regarding such matters but if you can afford it, legal guidance can help you achieve the best outcome.

Disclaimers

This article is general commentary on a topical issue and does not constitute legal advice. If you are concerned about any topics covered in this article, we recommend that you seek specific legal advice.

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure |

Image by Machel Jarmoluk via Pixabay

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Rachel Horan

Rachel Horan

Denise Raward

Denise Raward