Sydney’s property market entered 2022 leading the charge among Australian capital cities, with Domain data revealing property prices increased more than 33% over the course of 2021.

Peaking in the March 2022 quarter, ABS dwelling figures detailed Sydney recorded an average dwelling price of $1,227,200.

Since then it has been all downhill, with CoreLogic’s Home Value Index for November revealing an annual decline in property prices of 10.6%.

Domain’s Chief of Research Dr Nicola Powell noted when property prices fall it can understandably make many Australians feel uncertain about their property journey.

“It is important to remember that property has historically moved through upswings and downturns, and there are lessons that can be learnt from previous price cycles,” Dr Powell said.

“As per historical standards, the premium price point is showing the greatest weakness, clearly evident in the most expensive areas of Sydney and Melbourne.

“Premium-priced areas tend to lead price cycles, and while they may appear more vulnerable during a downturn, they see greater rates of price growth during the upward growth phase.

“This also means that when we move into a recovery phase, it will be evident first across the premium price-point.”

Of these premium price points, CoreLogic Economist Kaytlin Ezzy said suburbs in Sydney's City and Inner South, Northern beaches and Eastern suburbs regions dominated 2022's list for largest house and unit value declines.

“Houses in Narrabeen, Surry Hills, and Redfern recorded the most significant falls in value over the year, down more than 25%, while unit values in Centennial Park and Mona Vale fell by 23.1% and 20.8% respectively,” Ms Ezzy said.

Tome Avelovski, Director of Property Buyer’s Agency Ready Set Buy, said there are some good signs that we may be nearing the bottom of the cycle, as the rate of decline has eased over recent months.

“In Sydney, housing values fell by 2.3% in August, 1.8% in September and 1.3% in October,” Mr Avelovski told Savings.com.au.

“I expect prices will continue to soften over 2023 (up to -10%), as people adjust to higher interest rates, especially those coming out of record low fixed rates, however I do believe we’ll begin to see momentum pick up in the first half of 2024 with prices set to rise again.”

Mr Avelovski says once interest rates eventually stabilise, and inflation remains under control, we’ll see another surge of buyer activity and the next property ‘boom’.

“Sydney’s property market has historically been one of Australia’s strongest performing housing markets, with property values growing by 449% in the past 30 years,” he said.

“Remember, property is a long-term commitment and we’re in a buyer’s market now, where we have more leverage and negotiating power.”

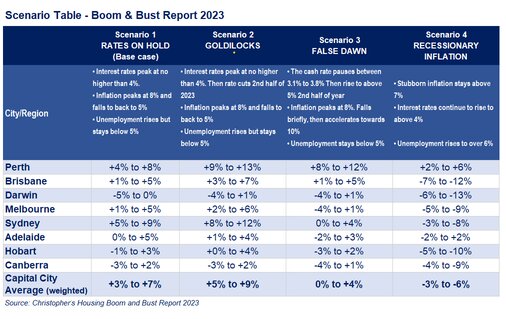

SQM Research Director Louis Christopher forecasts Sydney property prices could lift between 5 to 9% in 2023 if economic forecasts prove to be correct.

“Of course, it's largely centered around what inflation does and how the RBA responds,” Mr Christopher said.

Banksia, 2216

Banksia is located 16.3km from Sydney’s CBD and is considered by locals to be incredibly family-friendly, lying in close proximity to both beaches and the CBD.

PRD Chief Economist Dr Asti Mardiasmo views Banksia as an affordable and liveable suburb projected for growth in 2023.

“Banksia offers an annual median price growth of 1.8%, with $191.7 million in projects being injected into the area,” Dr Mardiasmo said.

“The key project for the area is the Princes Highway Mixed Use Development at a cost of $17.2 million providing 43 units.”

Banksia currently has a median house price of $1,490,000 based on PropTrack data.

Parramatta, 2150

Some 20km from Sydney’s CBD, the western suburb of Parramatta presents an opportunity for buyers in both the house and unit markets.

“Parramatta offers an annual median house price growth of 4.7% for houses and 1.7% for units,” Dr Mardiasmo said.

Parramatta’s drawcard amenity is Westfield Parramatta Shopping Centre, yet future construction includes Powerhouse Parramatta - the largest cultural infrastructure project in NSW since the Sydney Opera House.

Powerhouse Parramatta intends to open from 2025, serving as a cultural hub, with a museum front and center to deliver international exhibitions, education and community programs.

PRD Research reveals Parramatta had a median house price in the September quarter of $1,425,000 and a median unit price of $600,000.

Marrickville, 2204

Hello Haus Founder Scott Aggett says the suburb of Marrickville, some 7km south-west of Sydney CBD, is an attractive prospect for buyers.

“This is due to the affordable median house price compared to Sydney, which is at $1,875,000, low vacancy rates of 1.0% and 10-year compounding growth rate at 8.5% p.a.,” Mr Aggett told Savings.com.au.

“Marrickville has come back 4.3% since its highs of June 2022, outlining an opportunity to get into a tightly held market at a discount.”

Marrickville is described as unapologetically grungy, eclectic, friendly and casual with a range of amenities including Marrickville Metro, Marrickville Markets, Illawarra Road and Marrickville Road precincts.

Marrickville has a current median house price of $1,875,000, with a median unit price of $782,500 based on PropTrack data.

Moorebank, 2170

Moorebank is a well-established suburb according to Mr Aggett, positioned within 35 minutes of the Sydney CBD and attractive to buyers due to its lifestyle factors and convenience.

“The median house price has only come back 0.8% since the peak in May 2022 and now sits at $1,220,000,” he said.

“Moorebank will always perform well due to extremely low supply levels, low vacancy rates of 1.31% and a 10-year compounding growth rate at 9.35% p.a.”

Moorebank has a growing demographic comprising of singles, professionals and young families with Moorebank Shopping Centre, Wattle Grove Village, Chipping Norton Market Plaza the key amenities in the area.

Moorebank has a current median house price of $1,220,000 and a median unit price of $705,000 based on PropTrack data.

North Richmond, 2754

North Richmond is the furthest of the suburbs away from Sydney’s CBD to make the list, some 67km north-west of central Sydney.

Founder of McGrath Realty, John McGrath, said North Richmond lies at the foot of the Bells Line of Road tourist drive to the picturesque Blue Mountains.

“Bushwalking trails and strolling through the fresh food markets will become regular weekend activities for homeowners in this suburb,” Mr McGrath said.

“Considered less historic than its neighbouring suburb, North Richmond’s variety of housing options — from small blocks, long established residential, to large acreages, and new housing estates (Redbank) — offers something for everyone.

“If value for money and a slower pace of life within the city is for you, then add this suburb to your list today.”

The Redbank project in North Richmond worth $1.8 billion will deliver 1,400 dwellings with amenities including its own town village, restaurants, specialty shops, large childcare centre and RSL Lifecare retirement village plus 80 bed nursing home.

North Richmond has a current median house price of $1,000,000 and a median unit price of $660,000 based on PropTrack data.

Botany, 2019

Lying 10 kilometres from Sydney’s CBD with access to nearby beaches and the airport, Botany remains a quiet achiever given its proximity to the heart of the city.

Director of Sales at Upside Realty James Kirkland said Botany is being described by some as Sydney’s new ‘Newtown’ with the emergence of boutique breweries, bakeries and a growing arts scene.

“With a median house price of $1,885,000, Botany has seen 7.1% growth in the past 12 months,” Mr Kirkland said.

“The area is proving popular with growing families, with good buying opportunities on decent sized blocks of land,” Mr Kirkland said.

Amenities such as Sir Joseph Banks Park along the foreshore offers Botany residents walking tracks, bushland, gardens, an oval and running track.

Botany has a median house price of $1,885,000 and a median unit price of $870,000 based on PropTrack data.

Penrith, Campbelltown and Blacktown

Ready Set Buy’s Mr Avelovski anticipates growth in western Sydney and south-west Sydney will continue in 2023, especially with Badgery’s Creek Airport set to begin operations in 2026.

“Many suburbs across western Sydney and south-west Sydney continued to see property price growth over 2022,” he said.

“These include Penrith (+12.88% houses, +7.92% units), Campbelltown (+18.58% houses, +3.19% units), Blacktown (+18.58% houses, +3.19% units) and Liverpool (+21.21% houses, 5.10% units) – just to name a few.

“Steady growth throughout 2023 is expected in these markets, as they’re much more affordable than inner-city markets.”

Upside Realty’s James Kirkland agreed with this projection, noting plenty is happening out in Sydney’s west to develop secondary Sydney cities.

“The Penrith CBD is undergoing extensive redevelopment, with the median house price growing 11.1% in the past 12 months to $894,000. Surrounding suburbs including Colyton and St Clair are also worth considering given they have larger block sizes,” he said.

“Ropes Crossing in the Blacktown LGA had the highest gross rental yield in Sydney for October 2022 at 4% return. With a median house price of $900,000 and 6.5% growth over the past 12 months it’s definitely one to watch in 2023.”

Mr Avelovski noted the Australian and New South Wales governments are also investing $4.4 billion over 10 years in the Western Sydney Infrastructure Plan (WSIP), with the Australian Government providing over $3.5 billion.

“The WSIP will provide better road linkages within the western Sydney region and benefit the region's growing population,” he said.

“This investment will relieve pressure on existing infrastructure and unlock the economic capacity of the region by easing congestion and reducing travel times.”

Image by Matt Hardy via Pexels

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Bernadette Lunas

Bernadette Lunas

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Aaron Bell

Aaron Bell