Roy Morgan research shows 1.5 million Australian mortgage holders are now paying above a certain portion of their after tax income into their home loan, between 25 and 45% depending on income and spending.

This number has risen by 642,000 over the past year after twelve of the last fifteen monetary policy decisions saw interest rates go up.

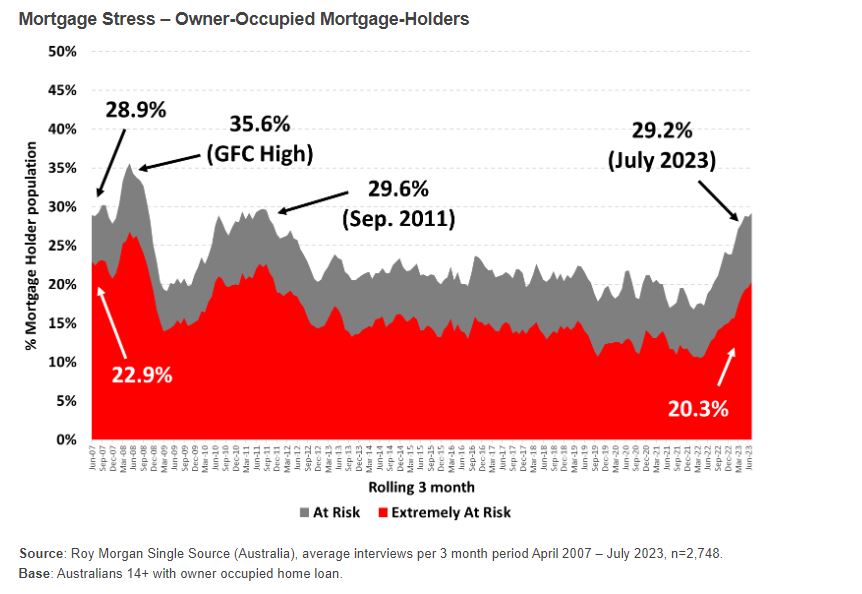

This exceeds the number of Aussies at mortgage stress at the height of the global financial crisis (1.496 million), although that was a bigger chunk of the population at the time.

Meanwhile, more than a million are 'extremely at risk' of mortgage stress, which means even if they were only paying interest, the repayments would exceed a certain proportion of household income.

This is the highest proportion of the Australian population at extreme risk since July 2008, and an increase of 470,000 people compared to the same time last year.

Roy Morgan CEO Michele Levine said the numbers were concerning, but pointed out interest rates were only one variable that influenced a household's ability to make their repayments.

"The variable that has the largest impact on whether a borrower falls into the 'at risk' category is related to household income, which is directly related to employment," Ms Levine said.

"If there is a sharp rise in unemployment, mortgage stress is set to increase towards the record high of 35.6% of mortgage holders considered 'at risk' in May 2008, during the GFC."

The unemployment rate has remained at historic lows throughout the high rate period, most recently moving up slightly to 3.7% for July, but the RBA expects the number to rise to 4.5% by December next year, as households tighten the purse strings, slowing growth.

How would more cash rate hikes change things?

Roy Morgan modelled the potential impact if the RBA were to raise the cash rate by another 25 basis points in both September and October, moving to 4.35% then 4.60%.

A September increase could mean a percentage point increase to 30.2% of Aussies with home loans at risk of mortgage stress, an extra 81,000 people to take the total to 1.577 million.

If the RBA, which by mid-September will be under the leadership of current deputy governor Michele Bullock, was to raise rates again in October, this would go up to 30.7%, or 1.6 million Aussies.

Of course, many analysts now feel we could be done with further hikes: the ASX RBA rate tracker as of 25 August suggested there was an 88% chance rates would stay at 4.10% in September, with 12% of the market expecting rates would be cut to 3.85%.

In August's monetary policy decision, current governor Dr Philip Lowe left rates unchanged for the second month in a row, and said the hikes that have already happened are working as intended.

"The higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so," Dr Lowe said.

CPI inflation dropped to 6% in June 2023, down from 7% in the year to March 2023, and current RBA forecasts suggest inflation is on track to return to the 2-3% target range by late 2025.

However, Ms Levine warns there are "new inflationary pressures" building in the economy, which could be upside risks to the cash rate target.

"During mid-August the average retail petrol price in Australia increased to over $2 per litre for the first time since July 2022," she said.

"On two occasions during 2022 average retail petrol prices increased to over $2 per litre. On both occasions after petrol prices soared inflation expectations also increased rapidly, up from 4.7% to 6.4% in March 2022 and up from 5.1% to 6.0% in July 2022."

"The increases to petrol prices are being driven by a decline in the value of the Australian Dollar which has now dropped below 65 US cents to its lowest for nearly a year since November 2022.

"As long as the Australian Dollar stays low and petrol prices stay high, and even increase further, there will be additional inflationary pressures in the economy."

See Also: Aussie Dollar to drop further to 62 US Cents

Personal insolvency also on the rise

Financial pressures are starting to bite more acutely across Australia, with personal insolvencies rising in the June 2023 quarter according to the Australian Financial Security Authority (AFSA).

There were 2,705 new personal insolvencies in the quarter, up from 2,301 during the same period last year.

In all state and territories, the numbers rose except for South Australia and Western Australia, where they remained steady.

AFSA Chief Executive Tim Beresford reminded Australians who are experiencing financial difficulty to look for help as soon as possible.

"Financial counsellors and registered insolvency practitioners can review your individual situation and help you to better understand the options available to help make a fresh start financially," Mr Beresford said.

Free confidential assistance is available through the National Debt Helpline or via phone at 1800 007 007.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by Andrea Piacquadio via Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!