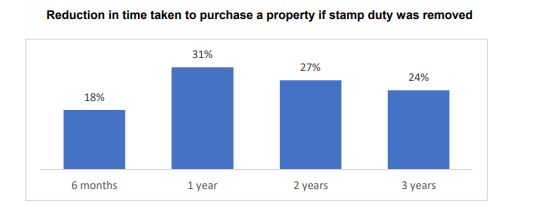

Gateway Bank surveyed 700 Australians who intend to buy their first property in the next four years and found over 60% would be able to buy a home sooner if they didn't have to pay stamp duty.

On average, first-home buyers (FHB) could buy a home 20 months sooner, while almost a quarter said it would reduce their homeownership timeframe by three years.

When asked about the biggest obstacles to purchasing their first property, 32% of FHBs said stamp duty and other fees were too high, ranking this as one of the top three barriers.

Buying a home or looking to refinance? The table below features home loans with some of the lowest variable interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

The research comes just a day after the New South Wales (NSW) government announced a proposal to axe stamp duty in favour of a land tax.

Gateway Bank Chief Executive Officer Lexi Airey said a smaller yearly amount to pay in tax instead of a large upfront payment would be preferable to most first home buyers.

“Stamp duty is a significant cost when buying a property, and can add years to the homeownership plans of First Home Buyers," Ms Airey said.

“While the NSW Government is proposing to replace stamp duty with a property tax, many first home buyers would be encouraged by any measure providing full or part relief from this upfront, one-off, cost.”

Source: Gateway Bank

Ms Airey added axing stamp duty could help FHBs who had experienced financial hardship as a result of COVID enter the property market.

“The proposed move to a new system stands to significantly fast-track the time to homeownership for first home buyers, and when combined with current government schemes, provides a range of support measures for those looking to get their foot on the property ladder.

"This will be particularly welcome news for many Australians who have had to utilise their deposit savings during the COVID-19 pandemic.”

Announced by the NSW Treasurer Dom Perrottet's budget speech yesterday, the proposal is designed to drive a post-COVID recovery.

Buying a house in Sydney at the median price of $1,154,406 would cost roughly $48,795 in stamp duty.

Mr Perrottet said axing stamp duty would remove one of the biggest hurdles to homeownership.

"Stamp duty is a relic from a bygone era when you picked one career, started a family, bought a home and basically settled in for life," Mr Perrottet said.

"It adds tens of thousands of dollars to the cost of the biggest financial commitment most people ever make."

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Rachel Horan

Rachel Horan