The 2021 Demographia International Housing Affordability report studied the rates of middle-income housing affordability in 92 major housing markets in eight nations.

Australia's major housing markets, Sydney, Melbourne, Brisbane, Perth, and Adelaide, were all rated as severely unaffordable, the third worst national market in the report.

Melbourne was rated the sixth most unaffordable city in the world for housing affordability, behind Auckland and Toronto but ahead of San Francisco, London, and Honolulu.

Buying a home or looking to refinance? The table below features home loans with some of the lowest variable interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Report author Wendell Cox said COVID had accelerated the trend of worsening affordability in major markets.

"In this year of the global pandemic and lockdowns, it is not surprising that housing affordability — given the large influx of new buyers, particularly in suburban and outlying areas — has continued to deteriorate," Mr Cox said.

"As a result many low-income and middle-income households who already have suffered the worst consequences from housing inflation will see their standards of living further decline."

Last year, regional housing values tripled the growth of their capital city counterparts, according to CoreLogic, which Mr Cox said may help to bring down prices in unaffordable markets.

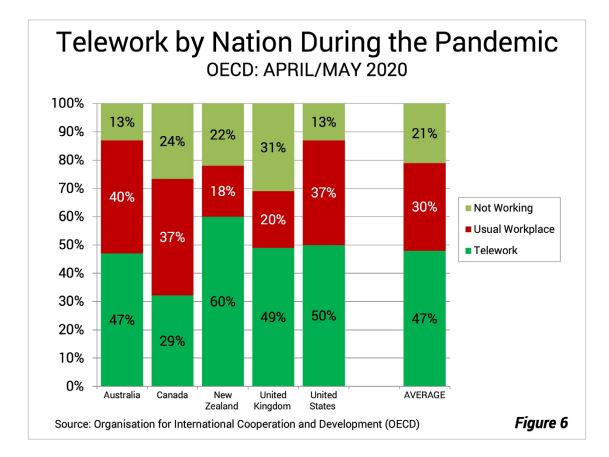

"The affordability issue is particularly critical due to the strong increase in remote working (telework) during the pandemic which is accelerating the movement to more affordable places," he said.

"It will likely also help flatten or even reduce prices in the highest cost housing markets as other households seek less costly housing elsewhere."

See also: Here's why Australian property prices didn't crash in 2020

Middle-class extinction?

The report found the deterioration in housing affordability represented an existential threat to the middle-income household.

"Higher housing costs relative to incomes are strongly correlated with higher overall costs of living and thus lower standards of living," it found.

"In the United States more than 85% of cost of living differences between metropolitan areas are reflected in housing cost differences.

"Similarly, Bloomberg reports that nearly all of London’s higher cost of living relative to the rest of the nation is associated with higher housing costs."

In a separate report, the Organisation for Economic Co-operation and Development (OECD) found “housing has been the main driver of rising middle-class expenditure,” with the largest increases in the costs of owning a home rather than renting.

“…the cost of essential parts of the middle-class lifestyle have increased faster than inflation; house prices have been growing three times faster than household median income over the last two decades," the OECD said.

The pandemic has only served to worsen conditions, with the report finding house prices had escalated, even though incomes had dropped among middle-income households.

"This is in large measure a result of substituting telework for physical commuting, which gave households the flexibility to seek new housing with more space, indoors and outdoors. This rapidly developing demand shock drove house prices up."

Working from home "a ray of hope?"

Despite driving up housing costs, many households were shielded in part from the fallout from COVID thanks to the working-from-home (WFH) shift.

The report noted that internet was now more important than a train line, in a shift that happened in days which in normal circumstances could've taken decades.

Mr Cox said greater remote working could begin to remove housing as a source of inequality.

"This could reduce housing demand in the least affordable areas, providing relief at every price point, including for many middle-income households whose living standards have declined as house prices have raced ahead of incomes," he said.

"It provides the global middle class a ray of hope."

See also: 30 Australian locations tipped to become working from home hotspots

Photo by Fidel Fernando on Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Alex Brewster

Alex Brewster

Rachel Horan

Rachel Horan