Since May last year, the RBA began its path to delivering the most aggressive rate hiking cycle in memory, lifting the cash rate from 0.10% to 4.10%.

And despite an interest rate pause this month, the RBA knife has well and truly been dug in.

While some may argue: rate hikes are what’s needed to contain inflation in a bid to reach the central bank’s 2-3% target objective, and borrowers need to hang in there for a bit longer, the reality is rising rates have hit Aussie mortgage holders the hardest.

Yes, the RBA has not pushed up its cash rate as much as other countries, but there’s an important difference between Aussie borrowers and borrowers in those countries.

| Country | Cash rate | Annual Headline CPI |

| Australia | 4.1% | 7% (March) |

| United States | 5-5.25% | 4% (May) |

| Canada | 4.75% | 3.4% (May) |

| New Zealand | 5.5% | 6.7% (March) |

| United Kingdom | 5% | 8.6% (May) |

Cash rates and CPI around the world as of 12/07/23

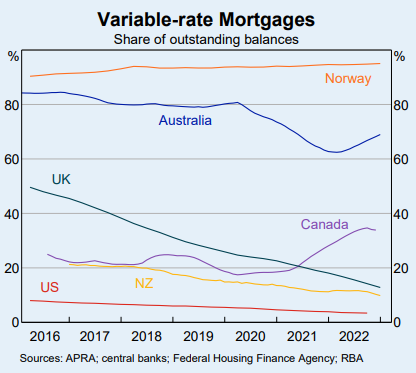

The variable-rate mortgage is our ‘go to’

Aussie borrowers absolutely froth a variable-rate mortgage. The Norwegians are the only country who use them more than us.

Roughly 70% of Australian mortgage holders are on variable rates. That’s compared to 35% in Canada, 15% in the United Kingdom, 10% in New Zealand, and less than 5% in the United States.

Fixed rates enjoyed their time in the sun in mid-2021 when more than half of all new mortgage commitments in Australia were on fixed rates - this was made possible by the RBA lending money to banks at cheap rates.

Now that's all flipped on its head, with fewer than 5% of mortage holders opting for a fixed rate in May 2023.

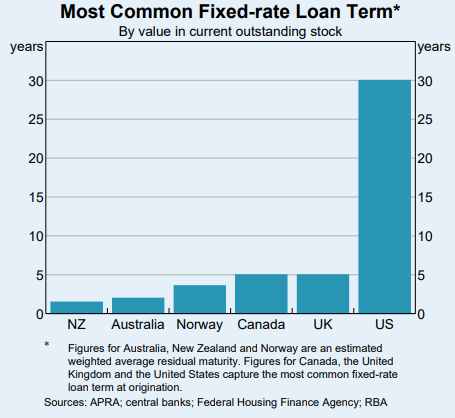

And while some Aussies do prefer the security of locking in a fixed-rate, the term is not for nearly as long as what’s considered ‘normal’ in the US - which is 30 years.

That's because in the United States, large pools of mortgages are underwritten by the government's mortgage agencies - Fannie Mae and Freddie Mac - making it easier for banks to offer fixed loans and to spread risk more evenly.

Imagine if you had locked in your interest rate back in the early 1990s. You’d still be paying off your home loan at 17.50%… You probably would have broken your fixed-rate by then though.

Even in the UK and Canada, the most common fixed-rate loan term is five years. That’s compared to the Australian average of about two to three.

So, while borrowers in other countries have a safety net (so to speak) around them with a fixed-rate, Aussie borrowers have been grappling with significant increases to their repayments over the past 14 months.

PRD Chief Economist Asti Mardiasmo said Australia has fixed terms for much shorter periods than most countries, which puts borrowers at a greater risk when there are changes in the cash rate and/or economic conditions.

“As new mortgage holders are offered short fixed-terms at different rates, our ability to predict mortgage costs is less and can fluctuate wildly,” Dr Mardiasmo told Savings.com.au.

“For example, a person with a three year fixed term can plan better than someone who is on a one year fixed rate, hence the fluctuation.

“Home loans make up circa 30% of our income, so a lesser ability to predict or plan for this will have a higher impact on household budget management. Making us feel the cash rate changes even more so than other countries.”

Even the RBA confirmed this.

“Interest rates on loans with very long fixed-terms tend to be less sensitive to changes in the short-term interest rates targeted by central banks,” the RBA said.

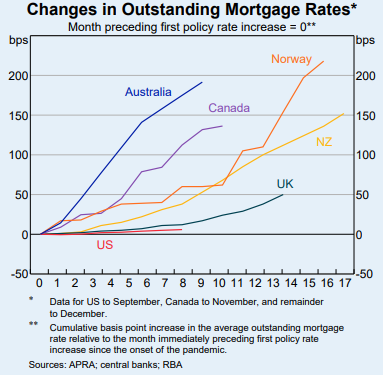

Rate rises pass on much quicker in Australia

Because most Aussies are on variable-rate mortgages, the increase in average mortgage rates has been far higher than those in other countries.

As the below RBA chart shows, the rates paid in NZ had climbed by just over 150 basis points, the rates in the UK by only 50 basis points, and the rates in the US by almost nothing at all.

If you look at Australia on the other hand, the rise in interest rates have hit households like a tonne of bricks.

Plus, with house prices increasing significantly over the pandemic years, mortgages themselves have become so much bigger than they used to be.

In January 2020, the average home loan size for an owner-occupier was $504,000. Fast forward to May 2023 and that figure is now $585,000; the peak was $618,000 in January 2022.

In other words, we’re paying a lot more in rates than we would have a few years ago, and bigger home loans have made us more sensitive to it.

It's thought that the popularity of fixed rates in the United States hampers housing mobility and ease of transaction, which partly keeps a lid on home price growth.

Incentives during the Covid-19 dark days

Variable-rate mortgages aren’t the only reason Aussies are doing it tougher.

According to Dr Mardiasmo, the boom in the number of home loan mortgages happened in a ‘triple threat situation.’

- The cash rate was at a historical low and money was cheap

- Policy initiatives such as the homebuilder and other buyer schemes were strongly pushed forward

- There was a perception/belief that property prices were declining due to the pandemic

“Other countries had point A and to a certain extent point B, but not necessarily point C,” she said.

“This is our differentiator, which when combined with points A and B created a cohort of home loan mortgagors that were quite precarious as they entered the market with very little deposit and safety net, had never experienced cash rate changes before and thus did not know how to plan for it, and were not expecting cash rate changes anytime soon.”

Not done yet

For Australian mortgage holders, the end is so close, yet so far away.

Markets and major bank economists are tipping at least one more rate hike in the coming months - either August or September, or both.

CommBank economists predict one last 25 basis point push next month to reach a peak rate of 4.35%. Meanwhile, ANZ, NAB, and Westpac each forecast a cash rate peak of 4.60%.

Either way, the mortgage pain will intensify and lift repayments even higher.

And with the next RBA Governor set to take Dr Lowe’s position in September, who knows what could happen.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by freepik

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Emma Duffy

Emma Duffy

Brooke Cooper

Brooke Cooper