Most of the growth was attributed to owner occupiers, surging 0.5 percentage points to 8.4% compared to the 12-month ended figure last month, while investment lending increased 0.3 percentage points to 2.2%.

The Annual housing credit growth figure is the highest since February 2018, while the owner occupier figure is the highest since October 2016.

By contrast, wages rose just 1.7% over the year, offset by trimmed mean inflation of 1.6%.

Westpac economist Andrew Hanlan pointed to another heady statistic.

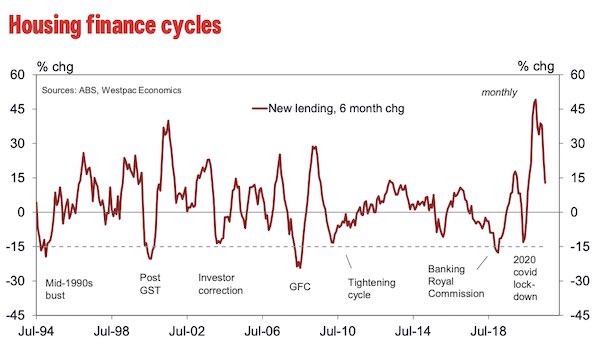

"Housing credit grew by 8.1% annualised over the three months to August. This includes a 0.62% increase in the month of August, which is an annualised pace of 7.7%," Mr Hanlan said.

"That is the fastest three month pace since April 2010.

"The sector was in a brisk upswing ahead of the latest lockdowns, responding to record low rates, the HomeBuilder program and a switch in demand as folk looked for more space at home.

"The RBA is closely monitoring developments in the housing market, with credit growth currently running ahead of that of household incomes."

ANZ economist Adelaide Timbrell echoed similar.

"The strength [is] still coming from owner-occupier borrowing. Even at these levels, housing credit will likely continue to outstrip income growth, which the RBA has consistently said is a concern for them," Ms Timbrell said.

The RBA's data comes after the Council of Financial Regulators (CFR) indicated yesterday it is reviewing current framework around lending conditions after strong property price growth through the year.

One of the policies tabled includes clamping down on lending to borrowers with debt to income ratios above six, which has surged this year.

New Zealand already has loan-to-value ratio restrictions - most owner occupiers need a 20% deposit, and most investors need a 40% deposit, or equity.

From Friday, Kiwi property investors will also be able to claim only 75% of their mortgage interest against their rental income, while certain 'bright line test' capital gains tax advantages will also be tweaked.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Photo by Steve Buissinne on Pixabay

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

.jpg)

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Harrison Astbury

Harrison Astbury

Dominic Beattie

Dominic Beattie