According to Roy Morgan research, NSW, VIC and the ACT saw numbers of those 'at risk' of mortgage stress tumble amid lockdowns.

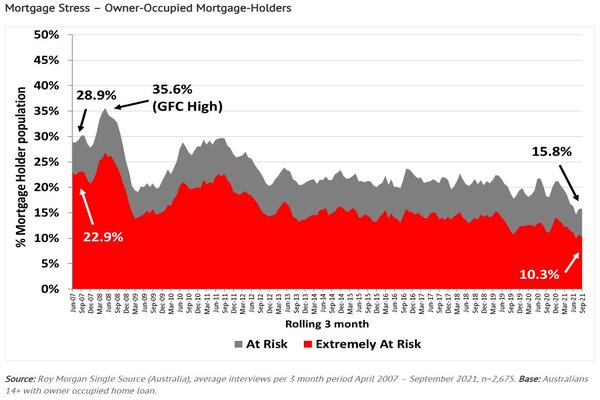

Throughout the three months to September 2021, Roy Morgan noted an estimated 584,000 mortgage holders (15.8%) were at risk of stress.

This is less than half the level it was during the Global Financial Crisis (GFC) in 2008 when it reached a high of 35.6% of mortgage holders.

According to Roy Morgan, this sharp drop was driven by a combination of record low interest rates, government financial aid and support offered by banks and financial institutions.

Roy Morgan Chief Executive Michele Levine said an analysis of economic factors and mortgages stress since before the GFC has shown that while the single biggest driver of mortgage stress is unemployment, interest rates and economic conditions have some impact on mortgage stress.

"The last year or so has seen low interest rates, but the real reason we see such low levels of mortgage stress is the Government support and mortgage deferrals for those mortgage holders who would otherwise have been at risk," Ms Levine said.

“The Federal Government’s ‘COVID-19 Disaster Payments’ have delivered over $11.9 billion to Australians in financial distress since June while APRA’s figures to September 30, 2021 show mortgages to the value of $11.5 billion have been deferred during the recent lockdowns."

Of the mortgage holders considered at risk in the three months to September 2021, Roy Morgan noted almost two-thirds, 357,000 or 10.3% of all mortgage holders, were considered extremely at risk.

This is down from 388,000 or 11.3% mortgage holders extremely at risk a year ago in the three months to September 2020.

Roy Morgan considers the risk of mortgage stress among mortgage holders in two ways:

- Mortgage holders are considered 'at risk' if their mortgage repayments are greater than 25-45% of after-tax household income – depending on income and spending.

- Mortgage holders are considered 'extremely at risk' if even the ‘interest only’ portion of their repayments is over a certain proportion of household income.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by Konstantin Evdokimov via Unsplash.

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Rachel Horan

Rachel Horan