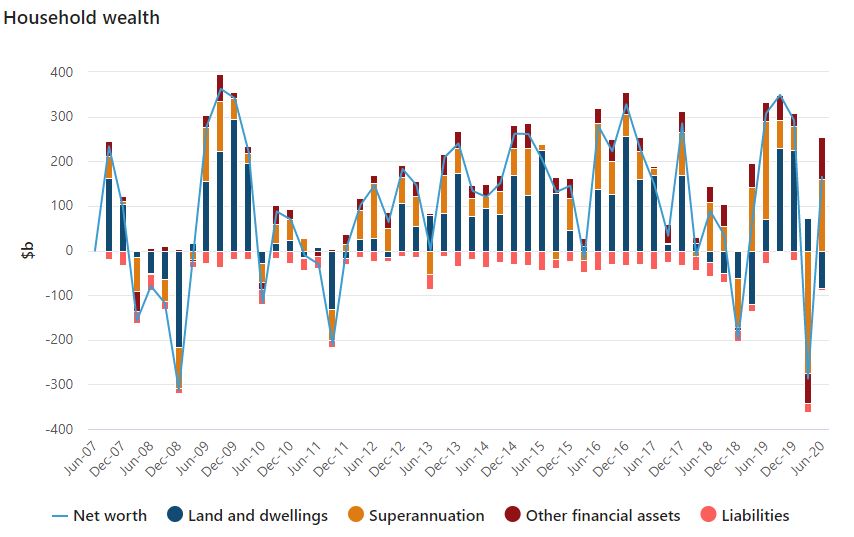

The figures from the Australian Bureau of Statistics (ABS) revealed a partial recovery from the 3.0% fall seen in the March quarter.

Strong sharemarket performance was the main driver of the increase, with superannuation balances (5.4%) and directly held shares (3.0%) posting strong growth.

Household deposits increased by $33.4 billion to be up 2.4%, as government income support packages like JobKeeper and early access to superannuation boosted many people's incomes.

Need somewhere to store cash and earn interest? The table below features savings accounts with some of the highest non-introductory and introductory interest rates on the market.

Special offer: Savings Accelerator (Kick Starter offer).

For a limited time, new ING customers can get a bonus 0.75% p.a on their savings rate balances of $150,000 up to $500,000 for the first 4 months. T&Cs apply.

If your balance is over $500,000 (but less than $5 million) you will earn the ongoing variable rate of 4.20%

Disclosure

Savings Accelerator

Special offer: Savings Accelerator (Kick Starter offer).

For a limited time, new ING customers can get a bonus 0.75% p.a on their savings rate balances of $150,000 up to $500,000 for the first 4 months. T&Cs apply.

If your balance is over $500,000 (but less than $5 million) you will earn the ongoing variable rate of 4.20%

All products with a link to a product provider’s website have a commercial marketing relationship between us and these providers. These products may appear prominently and first within the search tables regardless of their attributes and may include products marked as promoted, featured or sponsored. The link to a product provider’s website will allow you to get more information or apply for the product.

By de-selecting “Show online partners only” additional non-commercialised products may be displayed and re-sorted at the top of the table. For more information on how we’ve selected these “Sponsored”, “Featured” and “Promoted” products, the products we compare, how we make money, and other important information about our service, please click here. Rates correct as of July 13, 2025. View disclaimer.

Population growth helped total household wealth increase 1.5%, partially reversing the 2.5% fall felt in the March quarter.

Head of Finance and Wealth at the ABS, Amanda Seneviratne, said the figures demonstrated the bounceback in the economy as the nation grappled with the coronavirus.

"The June quarter 2020 financial accounts reflect the recovery of the Australian and international financial markets as the economic impacts of COVID-19 became more evident, and government and RBA policies took effect," Ms Seneviratne said.

Source: ABS

Many households used the pandemic as a way to get on top of their finances, with a $5.4 billion reduction of short term debt.

This reduction was driven by a continued trend of households using alternative methods of credit to credit cards, as well as paying down personal loans.

The largest offsets to household wealth were seen in house prices falling due to economic uncertainity and social distance measures, as well as a rise in housing loans.

There was an almost $84 billion fall in land and dwellings wealth and a rise of over $14 billion in housing loans.

The increase in loan amounts was driven by households taking advantage of record low interest rates to refinance mortgages to larger amounts, as well as interest accruing on deferred loan repayments.

Savings.com.au provides general information and comparison services to help you make informed financial decisions. We do not cover every product or provider in the market. Our service is free to you because we receive compensation from product providers for sponsored placements, advertisements, and referrals. Importantly, these commercial relationships do not influence our editorial integrity.

At Savings.com.au, we are passionate about helping Australians make informed financial decisions. Our dedicated editorial team works tirelessly to provide you with accurate, relevant, and unbiased information. We pride ourselves on maintaining a strict separation between our editorial and commercial teams, ensuring that the content you read is based purely on merit and not influenced by commercial interests.

Learn more about our commitment to editorial integrity in our Editorial Guidelines.

Our service is free for you, thanks to support from our partners through sponsored placements, ads, and referrals. We earn compensation by promoting products, referring you, or when you click on a product link. You might also see ads in emails, sponsored content, or directly on our site.

We strive to cover a broad range of products, providers, and services; however, we do not cover the entire market. Products in our comparison tables are sorted based on various factors, including product features, interest rates, fees, popularity, and commercial arrangements.

Some products will be marked as promoted, featured or sponsored and may appear prominently in the tables regardless of their attributes.

Additionally, certain products may present forms designed to refer you to associated companies (e.g. our mortgage broker partner) who may be able to assist you with products from the brand you selected. We may receive a fee for this referral.

You can customise your search using our sorting and filtering tools to prioritise what matters most to you, although we do not compare all features and some results associated with commercial arrangements may still appear.

For home loans, the base criteria include a $500,000 loan amount over 30 years. For car loans, the base criteria include a $30,000 loan over 5 years. For personal loans, the base criteria include a $20,000 loan over 5 years. These rates are only examples and may not include all fees and charges.

*The Comparison rate is based on a $150,000 loan over 25 years. Warning: this comparison rate is true only for this example and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

Monthly repayment figures are estimates that exclude fees. These estimates are based on the advertised rates for the specified term and loan amount. Actual repayments will depend on your circumstances and interest rate changes.

Monthly repayments, once the base criteria are altered by the user, will be based on the selected products’ advertised rates and determined by the loan amount, repayment type, loan term and LVR as input by the user/you.

Savings.com.au is proudly part of the InfoChoice Group, which includes InfoChoice.com.au, YourMortgage.com.au, YourInvestmentPropertyMag.com.au, and PerformanceDrive.com.au. The InfoChoice Group is associated with the Firstmac Group.

We may include products and services from loans.com.au, CarLoans.com.au, OnlineAuto.com.au, and YourMortgageBroker Pty Ltd, all associated with the Firstmac Group. Importantly, these brands are treated like any other commercial partner.

The information provided by Savings.com.au is general in nature and does not take into account your personal objectives, financial situation, or needs. We recommend seeking independent financial advice before making any financial decisions. Before acquiring any financial product, obtain and read the relevant Product Disclosure Statement (PDS), Target Market Determination (TMD), and any other offer documents.

Rates and product information should be confirmed with the relevant credit provider. For more information, read Savings.com.au’s Financial Services and Credit Guide (FSCG).

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Aaron Bell

Aaron Bell