On Monday, Treasurer Josh Frydenberg revealed a pre-Budget entrée announcing an expansion of the Home Guarantee Scheme with 50,000 places for three years from 2022-23.

The scheme now consists of three packages – First Home Guarantee, Family Home Guarantee, and Regional Home Guarantee - the latter of which is a new initiative aimed at helping those building in regional areas.

The expansion comes after a House of Representatives inquiry into housing affordability and supply revealed recommendations to improve both affordability and supply across the nation.

Delivering his Budget speech on Tuesday night, Treasurer Josh Frydenberg said the likes of HomeBuilder, the First Home Super Saver Scheme and the Home Guarantee Scheme have helped first home buyers.

“Over the last year, 160,000 Australians purchased their first home,” the Treasurer said.

“Helping more Australians to own a home is part of our plan for a stronger future.”

Pepper Money CEO Mario Rehayem said it’s pleasing to see the government back more Australians and open the doors to greater affordability, making it easier for Australians to get on the property ladder sooner.

“As these new or extended initiatives become available, more first home buyers will have greater opportunity than ever to secure a place,” Mr Rehayem said.

Peeling back the layers

AMP Capital Chief Economist Shane Oliver noted the housing measures announced by the Treasurer will result in higher than otherwise home prices - even though they are unlikely to prevent the cyclical downturn in prices now starting - and will boost debt levels.

“More home buyer incentives are unlikely to offset the negative impact of poor affordability and rising mortgage rates in driving a cyclical downturn in home prices,” Mr Oliver said.

CoreLogic head of research Eliza Owen also said these types of first home buyer schemes generally serve to boost demand "while protecting the value of homes" and current homeowners.

"Historically, targeted first homebuyer grants have incentivised buyers... the temporary boost to the first home owner grant increased housing activity around the time of the global financial crisis in 2008, when a lift in real estate transactions positively impacted the economy," Ms Owen said.

"Expanding the FHLDS [First Home Loan Deposit Scheme] could increase first homebuyer numbers at a time when the housing market outlook is uncertain. Alternatively this could increase demand for more affordable properties, increasing prices in this segment."

Real Estate Institute of Queensland (REIQ) CEO Antonia Mercorella welcomed the expansion of the Home Guarantee Scheme from 20,000 to 50,000 places a year, but expressed concerns over whether the measures went far enough to have a meaningful impact.

“While expanding the Home Guarantee Scheme is a good start and definitely a step in the right direction, it must be acknowledged that 50,000 places is not nearly enough to meet national demand,” Ms Mercorella said.

“Considering there were nearly 17,000 first home buyer loans in Queensland alone in the year to January 2022, and 36,000 first home buyer loans in Queensland alone last financial year, boosted by the HomeBuilder Grant, you can see how 35,000 places nationally is not going to make much of a dent on demand."

Speaking to Savings.com.au, PRD Chief Economist Dr Diaswati Mardiasmo echoed this sentiment noting these schemes only add to demand.

“There is no real solution offered yet when it comes to increasing housing supply, and although much of this does sit with the state and local councils, there is a need for better coordination between all levels of government to improve the balance of supply and demand,” Dr Mardiasmo said.

“It is a catch 22 as whilst it can assist those who are on the precipice of buying, it also adds to demand and ultimately without supply catching up it will push up prices meaning we may end up in a circular motion.”

CEO of RentBetter Jeremy Goldschmidt believes the extension of the First Home Buyers Scheme will help generate demand, yet the Government needs to be realistic about the growth in the property sector.

“Median house prices in Sydney and Melbourne are roughly $1.6 million and $1.1 million respectively. Ideally, the cap should be raised closer to these figures to meet the market, which has skyrocketed in the past 12 months,” Mr Goldschmidt said.

These prices have presented constant deposit barriers for first home buyers, with a Domain report noting it can take young couples up to eight years to save for an 'entry level' home.

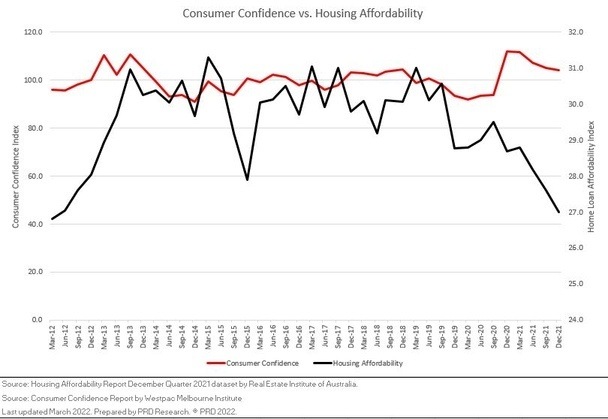

How does consumer confidence impact housing affordability?

Analysing the relationship between consumer confidence and housing affordability, Dr Mardiasmo noted they respond to each other in a cyclical manner.

“The relationship is cyclic, in the sense that any housing affordability reading can impact consumer confidence, and any new taxes or policies that impact consumer confidence can impact property demand and therefore housing affordability,” Dr Mardiasmo said.

“Consumer confidence as of March 2022 was at 96.6 index points, which is under the 100 positive index points reading, and it represents a declining trend.

“This should mean that consumers are less likely to spend on goods and services, which could potentially also mean property, yet a high concentration of first home buyer activity may not see the traditional level of drop in demand that is caused by lower consumer confidence.”

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by Ian MacDonald via Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Rachel Horan

Rachel Horan