Australians lose more money to gambling in the world than anyone else, throwing away over $US900 per capita each year according to a 2017 study. Meanwhile, Queensland Treasury stats report Australians collectively bet around $250 billion (with a b) each year and lose almost $25 billion. The COVID-19 pandemic didn’t help, with poker machine profits surging by more than $2 billion in New South Wales alone from June to November 2020.

Gambling is very accessible in Australia, and it costs the economy billions each year. A 2017 Bank Australia survey found 76% of Australians think banks bear some responsibility to minimise gambling harm using their cards, with credit cards being the biggest reason. With this in mind, Savings.com.au has compiled a list of banks and credit card companies that either ban gambling or allow customers to block it themselves, to help people maybe manage their gambling a little bit better.

The list of banks and credit cards that block gambling

The table below shows a summary of the Australian banks and providers that ban or partially block gambling transactions on either credit or debit cards.

|

Bank/provider |

Gambling banned on debit card? |

Gambling banned on credit card? |

|---|---|---|

|

American Express |

N/A |

Yes |

|

ANZ |

No |

Yes (if above 85% of credit limit) |

|

Bank Australia |

No |

Yes |

|

Bank of Melbourne |

No |

Yes |

|

Bank of Queensland |

No |

Yes |

|

Commonwealth Bank |

Yes (optional) |

Yes (optional) |

|

Citibank |

No |

Yes |

|

CUA |

No |

Yes |

|

Macquarie Bank |

No |

Yes |

|

NAB |

Yes (optional) |

Yes (optional) |

|

Suncorp |

No |

Yes |

|

Virgin Money |

No |

Yes |

|

Westpac |

Yes (optional) |

Yes (optional) |

Savings and transaction accounts that ban gambling

Blocking gambling transactions on debit cards is less common than bans on credit cards, as the table clearly shows. That’s because this is a very new phenomenon. This trend only started in early 2020, when NAB introduced an in-app feature allowing customers to place a temporary block on debit card transactions for sports betting and online gambling.

“We recognise problem gambling remains a major challenge affecting the community and one that requires organisations, governments, and the community to work together to effectively address,” NAB Chief Customer Experience Officer Rachel Slade said at the time.

Commonwealth Bank and Westpac followed suit with similar options. According to Savings.com.au’s research, these are the only banks that offer such a feature on debit cards.

Credit cards that ban gambling

So far, the following credit cards don’t allow gambling transactions*:

-

American Express

-

ANZ (to a point)

-

Bank Australia

-

Bank of Melbourne

-

Bank of Queensland

-

Commonwealth Bank (optional)

-

Citibank

-

CUA

-

Macquarie Bank

-

NAB (optional)

-

Suncorp

-

Virgin Money

-

Westpac (optional)

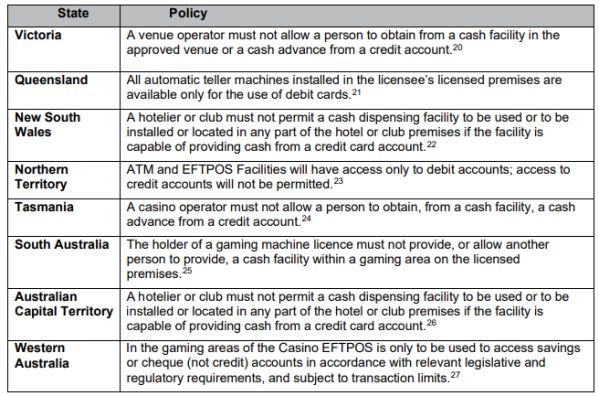

There are more credit cards that ban gambling at the moment compared to debit cards because there are already restrictions placed on the use of credit in gambling facilities. Between the years 2001 and 2003, all states and territories banned credit use in gambling venues.

Source: *Source: Australian Banking Association

This means that generally, no credit cards or cash advances can be used inside gambling areas such as gaming rooms at clubs. They also can’t be used at casinos or racetracks, but can still be used online and in betting apps as well as to buy lottery tickets. This is where the ban by certain banks comes in, although some may treat it as a cash advance, which can carry high interest charges and fees.

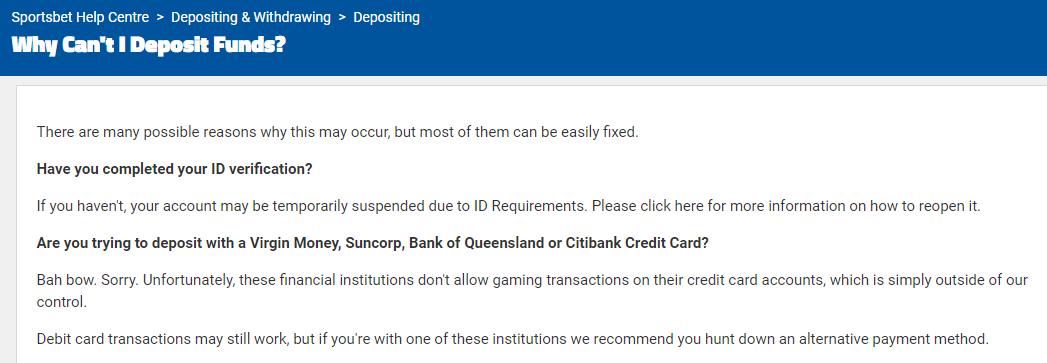

The blocks by certain credit cards also apply to online gambling as well as in-person gambling, as this FAQ from Sportsbet shows.

So technically by law, every credit card should block gambling at actual gambling venues. The cards we’ve listed just ensure you can’t do it online. Prior to the 2020 pandemic, 62% of gambling was conducted online among regular gamblers; during COVID-19, this increased to 78%, so this method is increasingly popular.

Should credit cards be banned for all gambling?

In a submission made to the Australian Banking Association (ABA), the Victorian Responsible Gambling Foundation (VRGF) said a ban on the use of credit cards to gamble would provide “a substantial and beneficial protection lacking since the rise of online betting.” According to the submission, 20% of online and racing gamblers are highly likely to experience harm, and were the most likely to use credit cards.

“Credit cards are of particular concern because they enable immediate and easy access to funds beyond those needed to meet an individual or family’s day-to-day living costs. Research shows that people who experience severe gambling harm are far more likely than others to gamble more money than they can afford; use credit cards to do so; and to access credit card funds early,” it said.

“Removing credit cards from this environment of constant incentives to bet will make a positive contribution to reducing gambling harm and the risk of gambling harm.

“By removing the ability to bet future funds, a brake will be applied to the speed and even extent of uncontrolled gambling.”

A 2010 Productivity Commission report, released at a time when online gambling was still fairly small, found problem gamblers were four times more likely to use a credit card, and were much more likely to have multiple credit cards, with one participant having 14 credit cards to gamble with totalling $300,000 worth of debt.

A more recent report by the UK found 47% of people who experienced gambling harm were credit card users - that’s nearly half. Those numbers are “not representative of typical credit card use” according to VRGF.

Seven of the 40 submissions from organisations made to the ABA were against removing credit card access to gambling, but these were from those tied to the industry such as Ladbrokes and Betfair. These organisations said banning all gambling on credit cards would:

-

Infringe on personal freedoms

-

Punish non-problem gamblers

-

Encourage illegal means to gamble

-

And wouldn’t address the underlying problems of gambling

However, people would still be able to gamble using cash or debit cards, and the UK survey found 50% of high-risk credit gamblers would start using their own funds if such a change occurred.

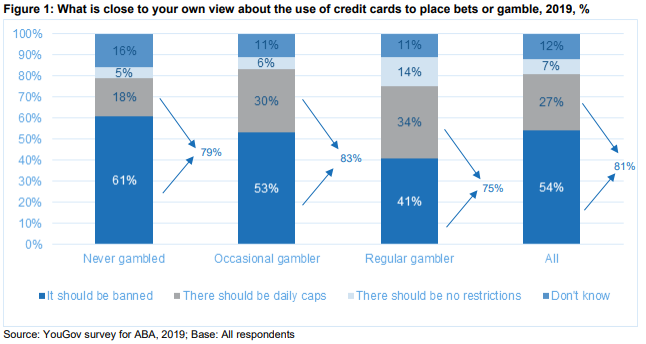

In terms of public opinion, a YouGov survey conducted for the ABA found only 7% of Australians think no restrictions should be placed on credit card gambling, while a combined 81% say it should be banned or partially banned.

Credit card debt can make gambling debt worse

One of the main issues with using credit cards to gamble is the high potential for added costs, due to the high fees and interest rates such cards often come with.

So using those nationwide gambling stats from before, we have enough gambling losses here for each person to lose $1,260. Now let’s compare that to the average credit card interest rate, which according to the Reserve Bank is a sky-high 17.24% p.a. That debt would take almost 11 years to pay off at twice the cost if you only made the minimum repayment.

It could be worse too, as you could build up much higher levels of debt and could have an even higher interest rate (many cards have rates well above 20% p.a!). In a joint-submission to the ABA, consumer organisations gave the following example:

“Minimum monthly payments on credit cards can mean that a debt can be very costly and take many years to repay. A debt-fuelled gambling binge therefore can result in years of financial detriment. For example, spending $10,000 in a night of gambling could take 43 years and 11 months to repay and cost $36,3324 if only making the minimum monthly repayments.”

VRGF found 76% of gamblers who used credit had built up debt due to gambling, far above the third of Australians who tend to build up credit card debt otherwise.

“Ongoing debt can lead to financial stress for the person who gambles and those close to them. This can act as a driver for some people to gamble even more – to chase their losses –and increase their debt,” a spokesperson told Savings.com.au.

“The use of credit to gamble can accelerate the speed and extent to which a person spends beyond their means.”

See also: How to cancel your credit card

Should more banks be limiting gambling with debit cards?

The Alliance for Gambling Reform (AGR) has previously called on more banks to step up after NAB introduced its gambling-block feature.

"Research has shown there are well over one million people in Australia experiencing gambling harm in some form, so something simple like this is very much needed," AGR Chief Advocate Reverend Tim Costello Costello said.

"Previously people could call the bank and ask for the same block, but NAB tells us this option was rarely taken up. This demonstrates why it's so important for other banks to offer similar anonymous options within their apps as soon as possible.”

These types of initiatives are not always actively promoted, and the ABA says it would not make any recommendations or force banks to implement them. Instead, it simply encourages banks to make their own decisions on these changes.

The Victorian Responsible Gambling Foundation also supports these measures.

“There is no one-size-fits-all solution to gambling harm, but one way banks can support at-risk customers is to give them the ability to block gambling transactions on their accounts. This is an option the Foundation supports, particularly for people who participate in race and sports betting.”

How to tell if you’re spending too much on gambling

Not everyone who gambles is classed as a ‘problem gambler’, or someone affected by gambling harm. Such a gambler may gamble frequently or infrequently - gambling is a problem if it causes problems in your life. According to various gambling resources, you might have a significant gambling problem if you experience any of the following, at which point you should check out the resources at the end of this article:

-

You feel the need to be secretive about gambling

-

You have trouble controlling your gambling (such as not being able to walk away)

-

You gamble even when you don’t have money (like with credit cards)

-

Friends or family have expressed concern to you

If you don’t meet these criteria, but like the odd gamble, it couldn’t hurt to do a review of your spending account to see exactly how much you’re flushing away each month. It may be more than you think.

“A financial review will identify whether money spent on gambling is proportionate to a person’s disposable income,” VRGF told Savings.com.au.

“However, money worries are only one indicator of gambling harm. Other signs include relationship problems; feeling stressed, anxious, ashamed or upset; losing track of time while gambling, and finding it difficult to concentrate on daily tasks.”

Savings.com.au’s two cents

If you want to minimise the amount of money you spend on gambling, then it could be a good idea to start using some of the products listed in this article. It can be very easy to rack up losses through gambling, especially if those losses are compounded by credit card debt that makes it all worse.

Applying for a bank card or credit card that blocks or cancels gambling transactions could be a good temporary solution. But for more serious cases, you should probably reach out to the experts.

Resources for gambling help

If you’re reading this and think you might have a problem with gambling, there are numerous resources you can reach out to for help and free, confidential advice and support.

-

Gambling help online:

1800 858 858 -

Lifeline: 13 11 14

Photo by Erik Mclean on Unsplash

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

William Jolly

William Jolly

Rachel Horan

Rachel Horan