The housing affordability crisis is worsening according to research from thinktank the Grattan Institute.

Data shows between 1981 and 2016, home ownership rates among 25-34 year-olds fell from more than 60% to 45%, and among the poorest 40% of that age group, it has more than halved, from 57% to 28%.

The Grattan Institute has proposed a shared equity scheme to help improve accessibility for first home buyers.

Under the proposed scheme, the National Housing Finance and Investment Corporation (NHFIC) would co-purchase up to 30% of the home value, taking a proportionate share of any profits when the home is sold.

Purchasers would borrow the remaining funds from a private lender, provided they have at least a 5% deposit.

Homeowners would also be able to buy out the government’s equity stake in 5% increments.

Income limits would be $60,000 for singles, and $90,000 for couples.

"A national shared equity scheme would help younger Australians get into the housing market faster, especially those without access to the ‘Bank of Mum and Dad’," the report said.

"Buyers would be able to borrow less for their first home – reducing the level of risk they take on – especially since interest rates are likely to rise from here.

"Other first home buyers may use the scheme to secure a larger home that can accommodate a growing family, avoiding the need to pay stamp duty twice if they upgrade in future."

In October last year the Victorian Government announced its own shared equity scheme, providing up to 25% of the purchase price for up to 3,000 applicants.

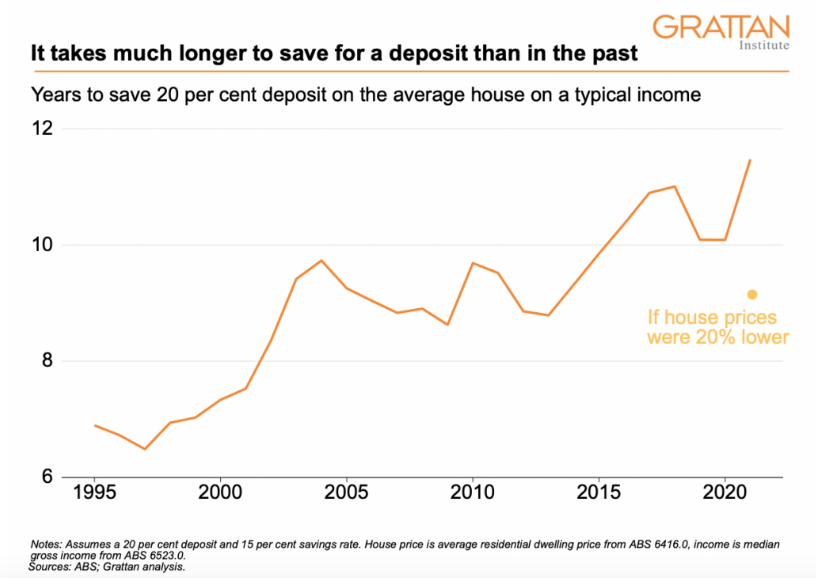

Time taken to save for a deposit blows out

According to Grattan Institute, home ownership rates are falling because it takes much longer today to save for a deposit.

"In the early 1990s it would take the average Australian about seven years to save a 20% deposit for a typical dwelling," the report said.

"Now it would take almost 12 years. Unsurprisingly, a growing share of Australians are relying on the ‘Bank of Mum and Dad’ for a deposit.

"Meanwhile older renters with a deposit won’t be in the workforce long enough to pay off a home by the time they retire, even at today’s record-low interest rates."

Source: Grattan Institute

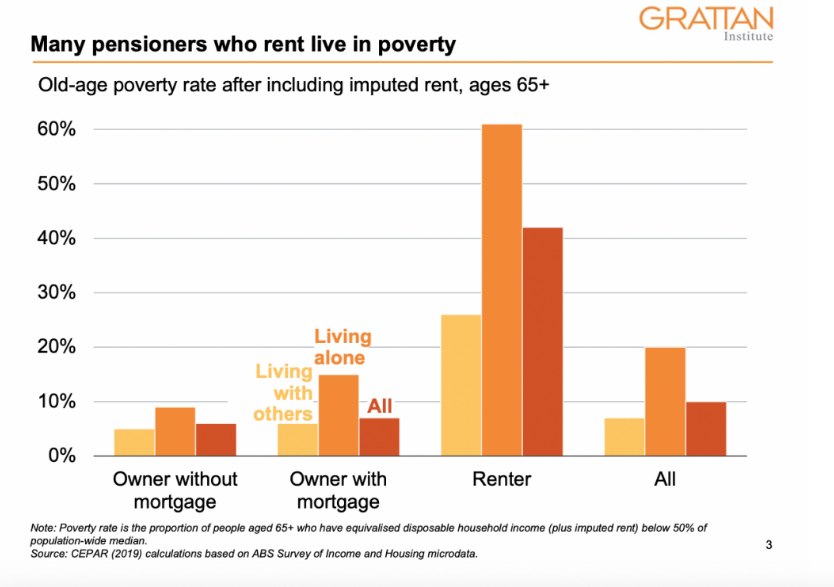

Shared equity for retirees?

The report from the Grattan Institute said without policy change, more retirees will rent in future.

Past Grattan Institute research estimates that by 2056, just two-thirds of retirees will own their home, down from nearly 80% today.

Mature aged borrowing has become a topical issue in Australia, as those who fail to break into the market in their 20s or 30s can struggle to get a home loan later in life.

According to Grattan Institute's report, senior Australians who rent in the private market are much more likely to suffer financial stress than homeowners, or renters in public housing.

"Nearly half of all retired renters are in poverty – with incomes below half the median," the report said.

"Their numbers will only grow as fewer retirees in future own their homes. Older women are especially vulnerable: women aged over 55 are already the fastest growing group to suffer homelessness in Australia."

Source: Grattan Institute

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by Barbara Horn via Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Arjun Paliwal

Arjun Paliwal

Jacob Cocciolone

Jacob Cocciolone