This comes as CoreLogic's national Home Value Index for December revealed a 1.1% drop, marking a reacceleration of property price decline following a softening in November.

Further, CoreLogic revealed prices are now down over 8% from their April 2022 peak, with an overall drop across 2022 of 5.3% to mark the steepest rate of property price decline in 14 years.

CoreLogic Research Director Tim Lawless said this has been a year of contrasts, with housing values mostly rising through the first four months of the year, but falling sharply as the RBA commenced the fastest rate tightening cycle on record.

“The more expensive end of the market tends to lead the cycles, both through the upswing and the downturn," Mr Lawless said.

This was the case for Sydney and Melbourne property markets which led the upswing throughout 2020 and 2021, before tapering back in 2022, falling by -12.1% and -8.1% respectively throughout the year.

Mr Lawless noted marginal gains in some regional areas including Regional South Australia have been able to withstand the 6.9% fall of seen across capital city dwelling prices.

“Regional SA has been the stand out for growth conditions over the past year, with values up 17.1% through 2022,” he said.

“The well-known Barossa wine region led the capital gains with a 23.0% rise in values over the calendar year.”

PropTrack's Home Price Index echoes the strength of the South Australian property market, revealing property prices excluding Adelaide are sitting 14.24% higher in December 2022 than December 2021.

| December % Change | 2022 % Change | |

| Sydney | -1.4 | -12.1 |

| Melbourne | -1.2 | -8.1 |

| Brisbane | -1.5 | -1.1 |

| Adelaide | -0.4 | 10.1 |

| Perth | 0.1 | 3.6 |

| Hobart | -1.9 | -6.9 |

| Darwin | -0.5 | 4.3 |

| Canberra | -0.2 | -3.3 |

| Capital city average | -1.2 | -6.9 |

| Capital city houses average | -1.3 | -7.4 |

| Capital city units average | -0.9 | -5.3 |

| Regional average | -1.0 | 0.1 |

| National average | -1.1 | -5.3 |

Source: CoreLogic Home Value Index - December 2022

AMP Chief Economist Shane Oliver said that the cash rate hikes the biggest driver of the slump and believes prices have a way to fall before they bottom out.

"We expect average property prices to fall further out to the September quarter 2023 as rate hikes continue to flow through and economic conditions deteriorate." Mr Oliver said.

"The full impact of rate hikes is yet to be fully felt as it takes 2-3 months for RBA hikes to show up in actual mortgage payments."

Given this factor, Mr Oliver believes further increases in mortgage rates will start to push total mortgage payments to record highs relative to household income.

"This is likely to result in a sharp rise in mortgage stress – particularly as fixed rate loans reset this year," he said.

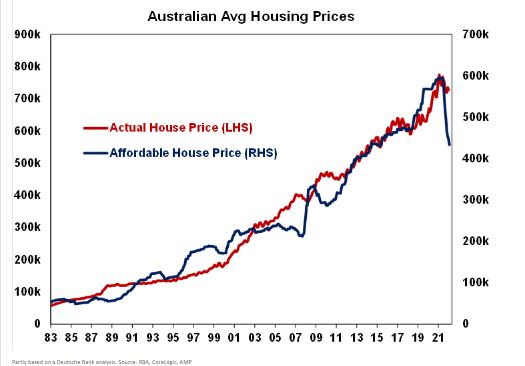

Further, Mr Oliver expects deteriorating economic conditions to see a large disparity between actual house prices and an 'affordable house price' estimate.

For reference, an 'affordable house price' is an estimate of the purchasing power of a buyer with a 20% deposit, average full time earnings and mortgage repayments at 28% of their total income.

"Over time home prices are tied to what people can afford to pay. But since April the amount an average new buyer can afford to pay has dropped by roughly 27% from around $600,000 to around $440,000. This demand side impact has been the key driver of home price falls so far, but suggests there is much more to go," he said.

Mr Oliver's current forecast remains for property values to bottom out at around 15-20% off their peak from April 2022, meaning Aussies can expect to see a further 9% decline in property prices throughout 2023.

CommBank economists back this view, expecting a 15% decline from the April 2022 peak, with fellow major bank economists less conservative.

NAB sees property prices declining to a total of 20% - the largest across major bank forecasts - while ANZ expects prices to decline to 18%, with Westpac at 16%.

Read more: House price forecasts for 2023 by the experts

Perth and Adelaide to buck the declining trend

Propertyology Head of Research Simon Pressley noted the best performers in 2023 are expected to come from outside of Australia's largest cities, yet expects to see a return to near-normal property market performance.

"The weakest locations will produce mild declines (between -2% and 5%)," Mr Pressley said.

"Candidates for this category are Ballina, Ballarat, Byron, Canberra, Kiama, Melbourne, Noosa, Sydney, Surf Coast and Warrugal.

"The strongest capital city markets in 2023 are likely to be Adelaide and Perth."

CoreLogic Home Value Index for December revealed throughout 2022, Adelaide grew 10.1% to take out first place, while Perth grew 3.6% to come in third behind Darwin.

No signs of rental crisis easing

Mr Pressley detailed 2023 will see a further squeezing of rental supply, as the government seeks to increase immigration to fill an estimated 500,000 jobs.

"The 8 million Australians who live in 3.3 million rental properties currently only have 31,924 dwellings to choose from if they need to move home for one reason or another," he said.

"Available rental supply is currently 58% less than it was 3-years ago. Expect more people to be sleeping in cars in 2023."

Mr Pressley believes alleviating the rental crisis will come down to which level of government has the 'kahoonies' to do the right thing and ease pressure on rental markets through introducing policies that support rental supliers.

"The 188,000 dwellings approved for construction this year is below the decade average of 202,000 per year," he said.

"Given that there is already near zero rental accommodation available, governments still face the choice of either introducing policies that incentivise more rental supply or to continue whacking property investors with the baseball bat, forcing even more people into makeshift shelters and homes," he said.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Picture by Mei Mei on Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Rachel Horan

Rachel Horan