Under the 'Super Home Buyer Scheme' commencing 1 July 2023, first home buyers will be able to invest up to 40% of their superannuation or up to a maximum of $50,000 to aid in purchasing their first home.

The Coalition notes this will mean Australians can buy their first home sooner by slashing the time taken to save a deposit by an average of three years.

Recent research from Domain revealed Aussies looking to enter the property market for the first time will need to save for up to eight years to afford a 20% deposit on a modest property.

The scheme is said to apply to both new and existing homes with the invested amount to be returned to the first home buyer's superannuation fund when the house is sold, including a share of any capital gain.

Prime Minister Scott Morrison said super should be harnessed to support the aspiration of many thousands of families who want to buy a home.

"It [the scheme] utilises money that’s currently locked away to transform a family’s life, with the money then responsibly returned to the super fund at the time of home’s sale," the Prime Minister said.

Minister for Superannuation Jane Hume said this is a two-for-one win for Australians - a home and a return on retirement savings.

“Superannuation is there to help Australians in their retirement, and the Super Home Buyer Scheme will ensure Australians can use those savings they are responsibly building up to improve their quality of life now and standard of living in retirement," Ms Hume said.

Speaking to Patricia Karvelas from ABC's RN Breakfast show Monday, Ms Hume revealed a 'bump' in house prices is expected if the Coalition is to win the election and the scheme is to come into play.

"I would imagine that their would be a lot of people that bring forward their decision to buy a house," Ms Hume said.

"So I would imagine in the short-term you would see a bump in house prices - but that doesn't play out the long-term benefits of more home ownership and fewer people relying on rent."

Federal Labor has rejected this policy, backing its own shared equity scheme.

Is cracking open your nest egg worth it?

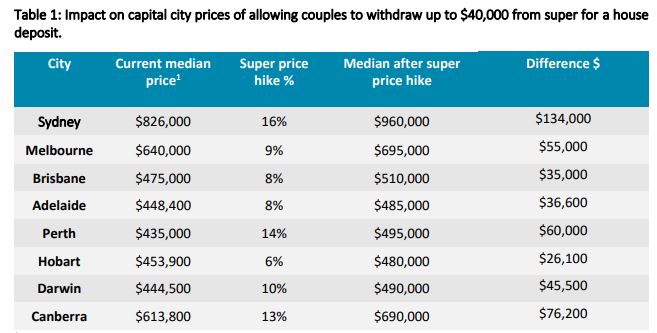

Industry Super Australia warns additional money Australians can take out of super via the scheme would almost immediately be gobbled up through housing price surges.

Modelling from the super body revealed utilising this scheme could hike the nation’s five major capital city median property prices by anywhere between 8-16%.

This analysis is based on an assumed take-up rate of the scheme from a combination of national consumer sentiment survey results and observed take-up of the COVID early-release super scheme.

Source: Industry Super Australia

Industry Super Australia notes by taking advantage of the scheme should it become available, many potential buyers would soon be locked out of the supercharged market, while others would be lumped with far bigger mortgages.

Industry Super Australia Chief Executive Bernie Dean said super is meant to be for people’s retirement, not supercharging house prices and pushing the home ownership dream further away.

"Throwing super into the housing market would be like throwing petrol on a bonfire – it will jack up prices, inflate young people’s mortgages and add to the aged pension, which taxpayers will have to pay for," Mr Dean said.

“Not only will it lock young people into hugely inflated mortgages without any requirement for their own deposit, it will torpedo investment returns for everyone leading to everyone having far less at retirement.”

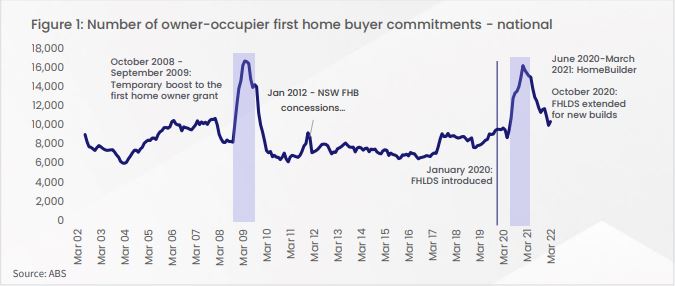

CoreLogic Head of Research Australia Eliza Owen said first home buyer activity has historically been elevated when first homebuyer schemes are enacted.

"It is a very challenging time to be incentivising more housing demand in the face of supply-side constraints," Ms Owen said.

Source: CoreLogic Property Pulse

Despite the supply constraints currently strangling the Australian property market, Ms Owen notes from ABS data the actual value that could be accessed through this scheme is relatively low for the typical young first homebuyer.

"First homebuyers are typically younger, and the median super balance was just $25,000 for those aged between 25 and 34 years of age. At 40%, the scheme would offer just $10,000 at the median level, or the equivalent of some state-based first homeowner grants," she said.

"CoreLogic data shows the current median dwelling value in Australia is $748,635, meaning the scheme could help increase the size of a standard deposit by around 1%.

"Those who would be able to withdraw up to $50,000 would have superannuation balances of $125,000. Unlike the first home loan deposit scheme, or Labor’s proposed shared equity scheme, there are no income caps associated with the Super Home Buyer Scheme, making it far more advantageous for young first homebuyers on higher incomes."

Non-bank lender WLTH's Head of Lending Catherine Mapusua echoes this sentiment believing the scheme will help those who already have a secure financial future, yet can assist in preparing for interest rate uncertainty that may lay ahead.

"As interest rates are expected to continue to increase in the near future, the need for a large deposit is emphasised further to avoid mortgage stress from overwhelming loan repayments," Ms Mapusua told Savings.com.au

"Having the Super Home Buyer scheme available will permit buyers to retain some of their cash savings, allowing a buffer or safety net for proposed interest rate increases.

"Even though this grant won’t directly rectify the [demand and supply] problem at hand, it is good to see another scheme made available to Australians."

Am I eligible?

The scheme will only come into play pending the Coalition winning the Federal election, which is held Saturday 21 May

The scheme would then commence 1 July 2023.

Eligibility criteria includes:

- Available only to first homebuyers who have separately saved at least a 5% deposit.

- Available to first homebuyers of any income.

- Each person in a couple may access the scheme if they are eligible.

- Applies to both new and existing homes.

- Applies to any property price.

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by Ashin K Suresh via Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Dominic Beattie

Dominic Beattie

Alex Brewster

Alex Brewster