The familiar tale of soaring property prices was felt across the nation throughout 2021, with residential property prices rising at the fastest pace annually since September 2003.

Over the year to the December 2021 quarter, Sydney and Melbourne recorded residential property price increases of 26.7% and 20.0% respectively. Since then, the property market across Australia’s largest capitals has begun to lose steam with Sydney and Melbourne posting price declines since March.

CoreLogic’s Home Value Index for May revealed Sydney housing values recorded the third consecutive month-on-month decline, down 0.2%, while Melbourne values were flat, down 0.04%.

Sydney and Melbourne hold the most significant weighting in the Home Value Index, which recorded a 0.6% monthly rate of growth - the lowest reading since October 2020.

CoreLogic’s Research Director Tim Lawless says the weakening state of the market has taken the rolling quarterly trend into negative territory across Sydney and Melbourne for the first time since these cities were in the midst of extended lockdowns in mid-to-late 2020.

See Also: How does a 20-something Melburnian spend their money on a $70k income?

What does a weakening market mean for homebuyers in Sydney and Melbourne?

Separated by state borders unlike Brisbane and the Gold Coast, PRD’s Affordable and Liveable Property guide revealed key insights into the performance of Sydney and Melbourne property markets throughout the first half of 2022.

Sydney

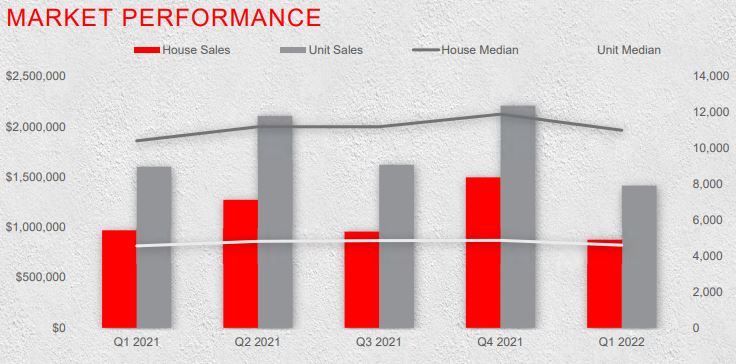

PRD revealed median property prices in Sydney Metro increased by 5.6% for houses to $1,965,000 from March quarter 2021 to March quarter 2022, and by 0.9% for units at $822,000.

Total sales declined 9.6% for houses between March quarter 2021 and March quarter 2022 while unit sales fell 11.7% over the same period.

In comparison PRD revealed between the September quarter of 2020 to the September quarter of 2021, Sydney Metro’s median price grew by 21.2% for houses and 9.8% for units.

During this period, the number of sales grew by 9.6% for houses and 21.1% for units.

PRD Chief Economist Dr Diaswati Mardiasmo said Sydney and Melbourne are becoming opportune markets for buyers and in particular first home buyers, with median property price growth either slower compared to the previous half of 2021 or swinging to a decline.

"The economy is entering a new phase of a higher cash rate and less fiscal and government stimulus meaning now is the time to transact," Dr Mardiasmo said.

Source: PRD Affordable and Liveable Property Guides for 1st Half of 2022 - Sydney Metro

Sydney suburb top suburb performers in 2021/22

| Suburb | Type | Median price 2020 | Median price 2021/22 | Price growth |

| Cammeray | House | $2,500,000 | $3,225,000 | 29.0% |

| Glebe | Unit | $839,000 | $1,088,000 | 29.5% |

| Willoughby | House | $2,395,000 | $3,050,000 | 27.3% |

| Cromer | Unit | $590,000 | $795,000 | 34.7% |

| Kurnell | House | $1,068,750 | $1,660,000 | 55.3% |

| Banksmeadow | Unit | $840,000 | $1,265,000 | 50.6% |

| Double Bay | House | $4,267,500 | $6,050,000 | 41.8% |

| Mosman | Unit | $1,000,000 | $1,200,000 | 20.0% |

| Gladesville | House | $1,910,000 | $2,531,000 | 32.5% |

| Hunters Hill | Unit | $967,500 | $1,235,000 | 27.6% |

Source: PRD Affordable and Liveable Property Guides for 1st Half of 2022 - Sydney Metro

Prices for Sydney rental homes rise 25% in March 2022 quarter

PRD revealed in the 12 months to the March 2022 quarter, the median house rental price increased by 25.0% to $750 per week. This growth remains at a faster rate than the median house sale price for the same period at 5.6%.

In March 2022, Sydney Metro recorded a vacancy rate of 1.6%, above Brisbane Metro at 0.7%. Sydney Metro vacancy rates have remained below the Real Estate Institute of Australia’s healthy benchmark of 3.0% for almost 12 months.

PRD notes this historically low vacancy rate, coupled with median rental price growth has the potential to create a 'confident' investment environment.

What Sydney suburbs are both affordable and liveable?

For both houses and units, Dr Mardiasmo says there are a number of definitions to define what is affordable, but ultimately affordability is individual, determined according to your needs and wants.

"These are not the cheapest suburbs, but these are the most affordable suburbs we could find that can fulfil all necessary criteria to offer a sufficient standard of living," Dr Mardiasmo said.

To determine a list of suburbs considered both affordable and liveable, PRD analysed a number of criteria including property trends, future project development in the area, affordability based on premiums on top of median prices and liveability.

Houses

If you're looking to buy a home in Sydney, PRD has highlighted three suburbs to consider based on select criteria:

- Miranda, 2228

- Peakhurst, 2210

- Riverwood, 2210

1. Miranda suburb profile

Miranda is located 20km from Sydney CBD, with a median house price of $1,640,000. This sits below Sydney Metro’s current median of $1,965,000.

For Miranda, annual median price growth is 27.0*%; rental vacancy rate (Mar-22) is 1.2%; rental yield (Mar-22) is 2.4%; total projects in the area are worth $88.0 million; and the unemployment rate is 3.0%.

2. Peakhurst suburb profile

Peakhurst is located 17km from Sydney CBD, with a median house price of $1,415,000.

For Peakhurst, annual median price growth is 22.8*%; rental vacancy rate (Mar-22) is 1.3%; rental yield (Mar-22) is 3.0%; total projects in the area are worth $17.1 million; and unemployment rate is 4.5%.

3. Riverwood suburb profile

Riverwood is located 17km from Sydney CBD, with a median house price of $1,200,000.

For Riverwood, annual median price growth is 20.0*%; vacancy rate (Mar-22) is 1.3 %; rental yield (Mar-22) is 3.0%; total projects for the area are worth $39.7 million; and unemployment rate is 4.5%.

Units

If you're looking to buy a unit in Sydney, PRD believes these three suburbs should be at the top of your wishlist:

- Telopea, 2117

- North Parramatta, 2151

- Wentworth Point, 2127

1. Telopea suburb profile

Telopea is located 17km from Sydney CBD, with a median unit price of $690,000.

For Telopea, annual median price growth is 6.2*%; vacancy rate (Mar-22) is 1.0%; rental yield (Mar-22) is 4.2%; total projects for the area are worth $12.0 million; and unemployment rate is 4.4%.

2. North Parramatta suburb profile

North Parramatta is located 20km from Sydney CBD, with a median unit price of $598,750.

For North Parramatta, annual median price growth is 2.4*%; vacancy rate (Mar-22) is 1.3%; rental yield (Mar-22) is 3.6%; total projects for the area are worth $14.9 million; and unemployment rate is 4.4%.

3. Wentworth Point suburb profile

Wentworth Point is located 13km from Sydney CBD, with a median unit price of $710,000.

For Wentworth Point, annual median price growth is 4.4*%; vacancy rate (Mar-22) is 1.4%; rental yield (Mar-22) is 3.6%; total projects for the area are worth $89.0 million; and unemployment rate is 4.4%.

*Median price growth captures sale transactions from 1st January 2021 to 31st March 2022, other figures current from March 2022.

Melbourne

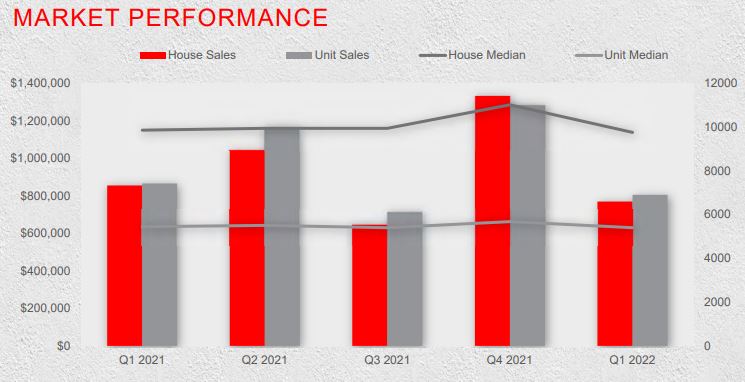

PRD revealed median property prices in Melbourne Metro softened 1.0% for houses to $1,140,000 from March quarter 2021 to March quarter 2022, and 0.8% for units at $630,000.

Total sales declined 10.0% for houses between March quarter 2021 and March quarter 2022 while unit sales fell 7.0% over the same period.

In comparison PRD revealed between the September quarter of 2020 to the September quarter of 2021, Melbourne Metro’s median price grew by 17.7% for houses and 2.4% for units.

During this period, the number of sales grew by a mammoth 73.0% for houses and 93.0% for units.

PRD notes the Melbourne Metro market has taken a turn in price growth, swinging to a higher level of affordability for buyers with demand - in particular for houses slowing, creating an opportunity for first home buyers.

Source: PRD Affordable and Liveable Property Guides for 1st Half of 2022 - Melbourne Metro

Melbourne top suburb performers in 2021/22

| Suburb | Type | Median price 2020 | Median price 2021/22 | Price growth |

| Kensington | House | $937,000 | $1,146,000 | 22.2% |

| Kensington | Unit | $532,000 | $552,000 | 3.7% |

| Greensborough | House | $795,000 | $1,000,000 | 25.8% |

| Greensborough | Unit | $640,000 | $718,000 | 12.2% |

| Moorabbin | House | $1,060,000 | $1,400,000 | 32.1% |

| Clayton South | Unit | $521,000 | $615,000 | 18.0% |

| Oakleigh South | House | $908,000 | $1,200,000 | 32.2% |

| Vermont | Unit | $725,000 | $845,000 | 16.6% |

| Altona | House | $920,000 | $1,185,000 | 28.8% |

| Taylors Lakes | Unit | $453,000 | $505,000 | 11.5% |

Source: PRD Affordable and Liveable Property Guides for 1st Half of 2022 - Melbourne Metro

Prices for Melbourne rental homes rise 15.2% in March 2022 quarter

PRD revealed in the 12 months to the March 2022 quarter, the median house rental price increased by 15.2% to $530 per week. This was complemented with a low 26 average days on the market.

In March 2022, Melbourne Metro recorded a vacancy rate of 1.9%, well above Brisbane Metro at 0.7% and above Sydney Metro at 1.6%. In similar fashion to Sydney, vacancy rates in Melbourne Metro have fallen to below the Real Estate Institute of Australia’s healthy benchmark of 3.0%.

What Melbourne suburbs are both affordable and liveable?

Houses

If you're looking to buy a home in Melbourne, PRD has highlighted three suburbs to consider based on select criteria:

- Greensborough, 3088

- Mulgrave, 3170

- Briar Hill, 3088

1. Greensborough suburb profile

Greensborough is located 17.6km from Melbourne CBD, with a median house price of $1,000,000.

For Greensborough, annual median price growth is 25.8%; vacancy rate (Mar-22) is 1.6%; rental yield (Mar-22) is 2.6%; total projects for the area are worth $34.0 million; and unemployment rate is 4.2%.

Greensborough was previously tipped by Dr Mardiasmo as a suburb to watch in December last year, with a median of $970,000 back in September quarter 2021.

2. Mulgrave suburb profile

Mulgrave is located 19.7km from Melbourne CBD, with a median house price of $1,000,000.

For Mulgrave, annual median price growth is 19.0%; vacancy rate (Mar-22) is 0.8%; rental yield (Mar-22) is 2.5%; total projects for the area are worth $8.9 million; and unemployment rate is 4.9%.

3. Briar Hill suburb profile

Briar Hill is located 19.1km from Melbourne CBD, with a median house price of $1,050,000.

For Briar Hill, annual median price growth is 19.1%; vacancy rate (Mar-22) is 1.6%; rental yield (Mar-22) is 2.6%; total projects for the area are worth $891,000; and unemployment rate is 4.3%.

Units

If you're looking to buy a unit in Melbourne, PRD believes these three suburbs should be at the top of your wishlist:

- Taylor Lakes, 3038

- Kensington, 3031

- Clayton South, 3169

1. Taylor Lakes suburb profile

Taylor Lakes is located 17km from Melbourne CBD, with a median unit price of $505,000

For Taylor Lakes, annual median price growth is 11.5%; vacancy rate (Mar-22) is 1.3%; rental yield (Mar-22) is 4.0%; total projects for the area are worth $39.1 million; and unemployment rate is 5.3%.

2. Kensington suburb profile

Kensington is located 4.0 km from Melbourne CBD, with a median unit price of $552,000.

For Kensington, annual median price growth is 3.7%; vacancy rate (Mar-22) is 1.9%; rental yield (Mar-22) is 4.7%; total projects for the area are worth $120 million; and unemployment rate is 5.2%.

3. Clayton South suburb profile

Clayton South is located 19.0km from Melbourne CBD, with a median house price of $615,000.

For Clayton South, annual median price growth is 18.0%; vacancy rate (Mar-22) is 1.5%; rental yield (Mar-22) is 4.3%; total projects for the area are worth $15.2 million; and unemployment rate is 5.4%.

If you would like to read the full reports, you can access them through the link here.

Image by Belle Co via Pexels

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward