‘Tobacco free’ finance isn’t refusing to give home loans to smokers, nor is it having an entire workforce being free of the black tar. Rather, it means that banks and other financial institutions won’t lend to or invest money in big tobacco companies. It’s a growing sub-sector of the market, so if you’re staunchly opposed to the tobacco industry, you might like to know where your money goes.

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers (these loans may not be tobacco free).

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Which financial companies are tobacco-free?

The world-leading organisation for tobacco free finance, ‘Tobacco Free Portfolios’, lists signatories that have taken the pledge to be tobacco-free. The organisation lays claim to in excess of US $11 trillion in assets under management. Overall there are 162 tobacco-free banks, lenders, super funds and insurers spread across 21 headquartered countries at the time of writing.

See also: Concerned about climate change? Consider switching your super

Australian (and Australia-present) finance and superannuation companies to have taken the pledge are:

|

Sector |

Tobacco-free companies |

|---|---|

|

Banking, Insurance & General Finance |

|

|

Superannuation |

|

Source: Tobaccofreeportfolios.org

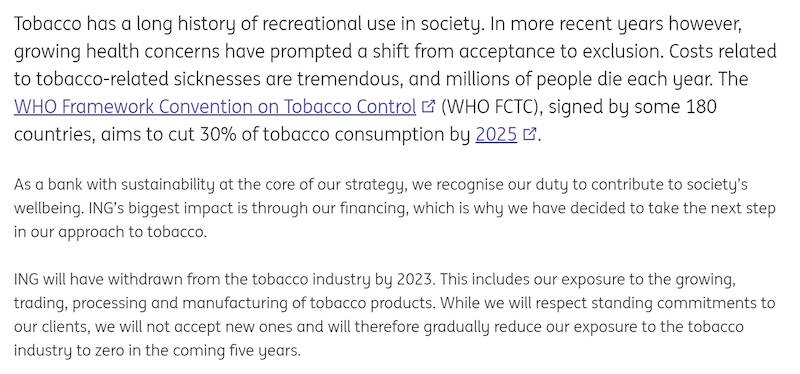

Some banks and lenders may still currently invest in and lend to tobacco, but have set deadlines to end this practice. Take ING, for example:

Source: ING

Does a tobacco-free investment portfolio hurt performance?

It’s a pretty common trope that a Birkenstock-wearing, granola-munching hippie might not be the best at investments. But a paper by Russell Investments indicates that tobacco-free investing and lending does not necessarily affect performance, is more widespread than you’d think, and is not necessarily done for ethical reasons.

The paper examined the role of tobacco in indices and active portfolios from 2003 through 2018, and found that active fund managers who sought to outperform the market chose not to include tobacco in their portfolios.

“This leads us to conclude that most managers don’t expect tobacco to outperform the broad market index,” the paper’s author said.

It also found United States-based large cap investors ‘underweight’ tobacco, meaning they invest in tobacco less than market availability.

“Roughly 50-70% of the [investing] universe avoids tobacco completely. While the existence of some tobacco-free portfolios is to be expected, the fact that 50% or greater exclude it directly strikes us as surprising,” the paper said.

“We believe this is unlikely related to client requests … It’s also worth pointing out that tobacco exposure has declined over the 2003-2018 period as well. This observation is less surprising, given the growing interest in excluding tobacco from portfolios in Europe and Australia.”

So, if active fund managers are avoiding tobacco industries not because of ethics but for performance reasons, what are the options for the everyday punter?

How to be an ethical investor

Well aside from quitting the darts yourself, there are presently a few investment options you could use to make sure your investment money isn’t going to the tobacco industry.

Apart from the companies listed earlier, there are a few ways to make tobacco-free investments, as well as ‘ethical’ investments such as climate-friendly portfolios, not investing in weapons companies and so on. One common way is through investing in exchange traded funds (ETFs), which are generally lower-cost than actively-managed funds.

Some ‘ethical’ ETFs available in Australia include:

-

ETHI: Betashares Global Sustainability Leaders ETF

-

VESG: Vanguard Ethically Conscious International Shares Index ETF

-

RARI: Russell Australian Responsible Investment ETF

-

Raiz: ‘Emerald’ Portfolio

This is not an exhaustive list, however all screen for companies that invest ethically, and aim to stamp out tobacco. Be aware that like the label ‘may contain traces of nuts’ in your food, the screening process might not capture all tobacco-free investments 100% of the time.

According to Raiz, responsible investments in Australia amounted to $866 billion in assets under management in 2018, making Australian investors one of the world leaders in the space.

“An analysis from MSCI [Morningstar] found that the performance of two portfolios screened to overweight stocks with higher ratings in environmental, social and governance (ESG) characteristics outperformed the global benchmark over the last eight years,” a Raiz paper said.

A large part of this is because many ESG stocks are technology companies such as Amazon, Google, and Apple, which have performed strongly over the last decade.

Always check the fees associated with ethical investment ETFs, as you should with any investment, and note that past performance is not an indicator of future performance. The floor is yours.

Savings.com.au's two cents

We’re not suggesting you have to invest in tobacco-free companies. You might have other priorities, and frankly, go for your life. Tobacco is, at the end of the day, a ‘free choice’ product. However, it is interesting to note there is some evidence to suggest fund managers are avoiding tobacco simply for performance reasons, and not for ethical purposes.

While ethical investments' performance can be attributed to being tech stock-heavy, it does seem like tobacco companies are being left in the dust, regardless of ethics. Nevertheless, before you jump into any investment or financial product, do your due diligence, not just on the ethics, but on the fundamentals, such as fees and costs.

Photo by Lex Guerra on Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

.jpg)