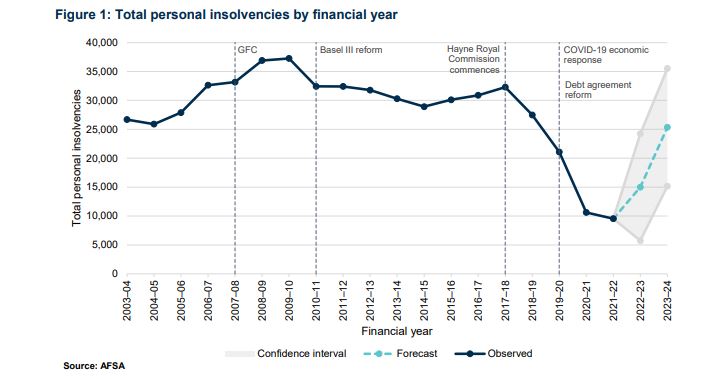

After historic lows in 2021-22 (9,545 in total), AFSA is preparing for increased levels of financial stress to result in significantly higher levels of personal insolvency.

The combination of continually rising interest rates, high inflation and soaring energy prices could overwhelm many vulnerable Australians with unpayable debts.

Already, AFSA has reported moderate increases in both informal insolvency arrangements and the number of people calling debt helplines to talk through credit card and mortgage repayments.

It also highlighted the fact that a number of Australians have fixed rate mortgages that expire between March and July this year as another potential risk factor.

The number of yearly personal insolvencies is expected to return to above 25,000 by 2023-2024.

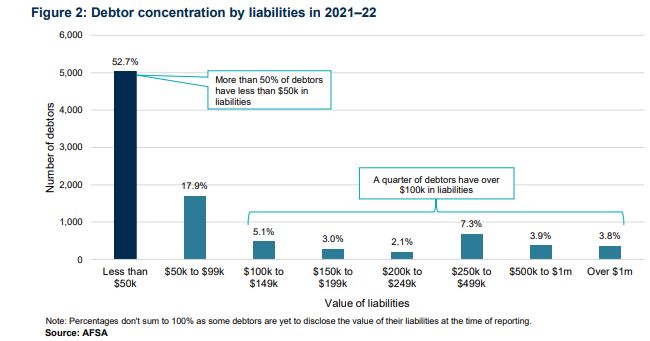

AFSA say there is currently nearly $18 billion worth of liabilities managed by the personal insolvency system.

This money is owed to a range of creditors, including the ATO ($2.1 billion) and the big four banks ($4 billion).

What is an insolvency arrangement?

Personal insolvency is a means to settle debts without being declared bankrupt.

If you have debts that are becoming insurmountable, you can enter a personal insolvency agreement, where a third party (trustee) takes control of your assets and negotiates terms with your creditors.

This can include a debt repayment plan in instalments, some of the debt being partially forgiven or your property being sold to cover the costs, depending on the terms of your agreement.

While this might seem like a process for those in millions of dollars worth of debt, the majority of people who entered insolvency in 2021/22 owed less than $50,000.

AFSA Chief Executive Tim Beresford said insolvency agreements "allow people in financial distress to get a fresh start, while providing a remedy for those who are owed money".

What caused the previous drop in insolvencies?

In 2009-10, after the Global Financial Crisis, there were 37,263 people declared insolvent in Australia.

Since then, several structural changes were made to the insolvency system to steadily push these numbers down.

Basel III regulations introduced worldwide in 2011 as a response to the GFC changed credit lending standards, decreasing the number of high risk loans.

In Australia, the Hayne Royal Commission into misconduct in the banking, superannuation and financial services industry had several recommendations that further influenced the way creditors both issued loans and recovered unpaid debts.

During Covid-19, the government introduced several measures to reduce financial hardship, including temporary debt relief legislation, government stimulus packages and debt repayment holidays from industries.

Mr Beresford said that further reforms to benefit both creditors and debtors are a possibility later this year.

"We are aware that many of our stakeholders are interested in potential personal insolvency reforms," Mr Beresford said.

"As announced by the Attorney-General, the Government is keen to explore pressure points of the current personal insolvency system, critical reform areas and longer-term priorities."

Picture by Nicola Barts on Pexels

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

William Jolly

William Jolly

Harrison Astbury

Harrison Astbury