Before we launch into what compound interest is, maybe we should start with a brief explanation of what interest means in the world of finance. If we’re talking about savings accounts, for example, interest is money paid to you by the bank as a reward for entrusting them with your money. It’s also an incentive for you to continue to entrust them with your hard earned cash.

The interest the bank pays you is directly proportional to the amount of money you have deposited, as well as the interest rate.

Need somewhere to store cash and earn interest? The table below features savings accounts with some of the highest non-introductory interest rates on the market.

Provider | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 200 | 0 | $product[$field["value"]] | $product[$field["value"]] | $product[$field["value"]] | More details | |||||||

| No monthly fees | Save Account

| ||||||||||||

Save Account

| |||||||||||||

| 0 | 1000 | 0 | $product[$field["value"]] | $product[$field["value"]] | $product[$field["value"]] | More details | |||||||

Savings Maximiser (<$100k) | |||||||||||||

| 0 | 1000 | 0 | $product[$field["value"]] | $product[$field["value"]] | $product[$field["value"]] | More details | |||||||

Boost Saver | |||||||||||||

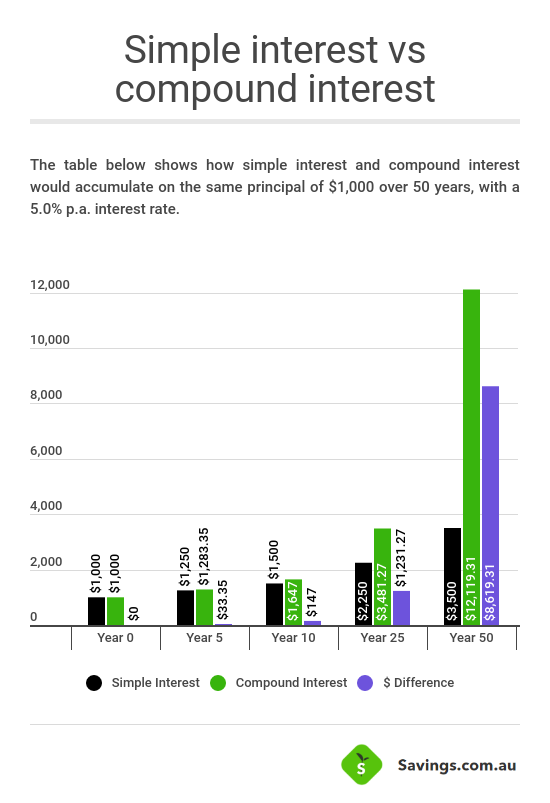

There are two main types of interest: simple interest and compound interest. Simple interest is paid at the end of a specified term, but if the term is longer than 12 months, interest may be paid annually. With simple interest, the interest rate is applied to the principal only. A term deposit is an example of an account that often earns simple interest.

Now we’ve got that out of the way, let’s move on to what compound interest is and how it works.

What is compound interest?

At its most basic level, compounding is the process of growing or building upon itself – the snowball effect!

Compound interest is interest paid on the initial principal (the original sum of money you’ve invested, or the amount borrowed or still owing on a loan), as well as the accumulated interest on money you have invested or borrowed. Compound interest is basically the equivalent of double chocolate topping – but for your savings instead of your bowl of ice-cream. You earn interest on the money you deposit, and on the interest you’ve already earned – in other words, you earn interest on your interest. It’s almost better than double chocolate topping.

Put simply, compounding interest means you earn interest on your interest. So while you have to hustle to earn the money you initially invest, from there on the money does all the hustling for you. A double sugar hit for your savings!

To get the most out of compounding interest, there are three golden rules:

- Reinvest (save) the interest

- Think long term

- Keep adding money

One of the key ingredients in compounding interest is time.

Throw time into the mix and compounding becomes a serious money-making weapon. The longer you leave your nest egg to grow, the bigger the effects on your money.

Take this as an example: A 20-year-old would only need to save and invest $1,000 of their annual pay in fortnightly instalments, and they’d be a millionaire by the age of 40 (this assumes a modest return of 7% p.a.). That’s a whopping $642,341 you’ve earned in interest and investment returns on top of the $520,000 you’ve deposited over a 20-year period (according to ASIC’s compound interest calculator). Not bad.

As you can see, the longer you leave your money to grow, the more money you accumulate thanks to the magic of compounding interest.

How to calculate: compound interest formula

There are a few ways you can calculate compound interest.

Online calculators are probably the easiest way to calculate compound interest as they do all the maths for you and can create charts and year-by-year tables, allowing you to see how much money you’ll have if you regularly save.

If you’re determined to put your math skills to the test, you can do your own compound interest calculations by using this equation:

A = P x (1 + r)n

Formula explanation

A = the end amount of your investment

P = the principal (the starting amount)

r = the percentage interest rate converted to a decimal rate (e.g. 2% is 0.02)

n = the number of time periods

In most cases, the interest will be compounded monthly (12 times a year) for a standard savings account, and annually if you’re trying to calculate the interest earnings on a long-term deposit.

How do the banks calculate compound interest on my savings account?

The banks typically calculate interest on the daily closing balance. This is the equation for savings accounts:

Daily closing balance x interest rate (as a percentage) / 365

Interest begins to accumulate on the day the opening deposit is made into your savings account. Then, it’s credited to your account on the last day of the month. Generally, any interest that’s awarded to your savings account is available for use on the same day it’s been credited.

How do I know if my savings account is paying compound interest?

Most, if not all, savings accounts pay compound interest.

To find out if your savings account is paying compound interest, you will want to take a look at when the interest is paid and where. Interest that is paid monthly into your savings account will be compounded.

If your savings account requires a minimum monthly deposit, any interest you earn generally won’t count towards that as the minimum monthly deposit requirements must be met with other funds.

How can you make compound interest work for you?

Just like getting over a breakup or waiting for your fiddle leaf fig to grow, when it comes to compound interest – it takes time. It’s an effective way to build enormous wealth, but it’s definitely not a get-rich-quick scheme.

The sooner you understand the power of compound interest, the sooner you can put it to work for you.

Save early and often

If you haven’t already figured out the blindingly obvious by now, time is money when it comes to compound interest. Get into the mentality that the longer your money earns compound interest, the better. We’re talking decades, not just a few years.

In some cases, saving earlier can mean you don’t need to save as much money as somebody who waits to start saving. And even if you quit saving at some stage, your head start will continue to pay dividends later.

Look at the interest rate

Many savings accounts offer a standard rate paid on the entire balance, no strings attached, plus a bonus interest rate you’ll only get if you meet certain criteria. It’s an incentive designed to stop you from touching your savings which will help your compound interest grow, which is why you should:

Keep your savings separate from your spending money

A pitfall of using your savings account to grow your compound interest is how easy it is to access your money.

To stop yourself from dipping into your hard-earned savings, pop them away into a separate high-interest savings account and try not to touch them at all.

The ugly side of compound interest

Compound interest is all peachy – until you’re the one paying it if you have loans or any other outstanding debt (it’s what makes credit cards so hard to pay off!).

The majority of loans and line of credit products offered by banks and credit unions (think home loans, credit cards, car loans) charge compound interest.

When you’re borrowing money, compounding interest works against you because you’re paying interest on the money you’ve borrowed.

Unless you diligently pay off your credit card in full at the end of each month, compounding interest can make the outstanding balance get bigger and bigger as time goes on. If being unable to afford to pay off the credit card balance was the reason it was outstanding in the first place, the balance growing bigger because of compounding interest is a recipe for financial ruin.

Compounding interest is just one of the many reasons why knowing how much you can realistically afford to borrow is so important. Compound interest is great when it’s working for you but a right royal pain when it’s not.

Savings.com.au’s two cents

Compound interest is one of the most important financial concepts to understand if you want to watch your money grow. Having a good grasp on what compound interest is and how it can boost your savings is something we think everyone needs to know. If you can understand the benefits of compound interest earlier in life, you’re a lot more likely to reap the rewards of it later on.

Similarly, if you can understand the less shiny side of compound interest, you’re more likely to make compound interest work for you, not against you.

If you don’t already have a savings account, open one right now – it can take as little as ten minutes online. Pick a savings account with a high interest rate and start depositing money. It doesn’t matter if your initial deposit is small – it’s all about having time on your side and using that time, as well as making regular deposits, to harness the power of compound interest.

Jacob Cocciolone

Jacob Cocciolone

Denise Raward

Denise Raward