In an effort to stop soaring inflation, the RBA has had ‘no choice’ (in their eyes) but to push the cash rate to 4.10%, lifting the average new variable interest rate for owner occupiers from a low of 2.41% p.a. in April 2022 to 5.94% p.a. in June 2023.

In June, an estimated 1.43 million Aussies - nearly 29% of mortgage holders - were ‘at risk’ of mortgage stress according to Roy Morgan research.

That is half a million more than a year ago.

Even the average fixed-rate home loan is too high to offer borrowers much of a reprieve from rate hikes.

And with some lenders raising both variable and fixed rates over the last few weeks on their own terms, what other options are available?

Enter a capped-rate home loan.

How does a capped-rate home loan work?

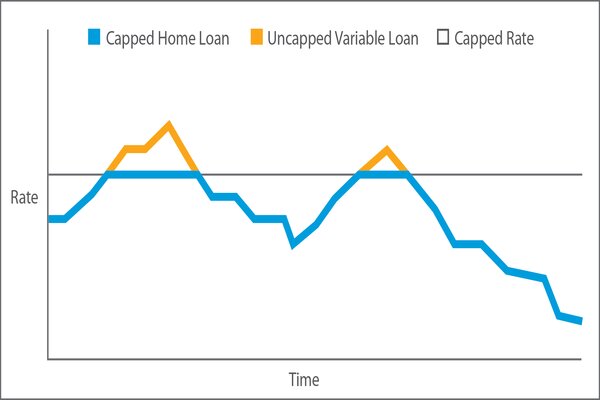

A capped-rate home loan is a mortgage that has a built-in rate ceiling for a certain period of time, meaning no matter how much rates rise, the interest rate cannot surpass the cap.

To give you an idea, here’s an example:

Capt. Rate has a capped-rate home loan. The cap rate is 7% p.a. and the capped period is three years.

Capt. Rate’s interest rate cannot go above 7% p.a. during the first three years of the loan, even if the RBA lifts the cash rate.

Essentially, a capped-rate home loan is like a variable-rate home loan, but provides a barrier that prevents the interest from exceeding a certain point. You could think of it like a safety net.

Which lenders offer capped-rate home loans?

While capped-rate home loans are rare, one Australian customer-owned bank has recently launched one.

Northern Inland Credit Union’s (NICU) Capped Home Loan is designed with rate hikes in mind.

The loan has a rate cap of 6.04% p.a. (6.39% p.a. comparison rate*) for a three year period.

The loan’s features include a redraw facility (minimum redraw of $500) and a 100% offset account.

Fees include a $600 establishment fee and $350 annual fee.

The Capped Home Loan product is available for mortgages with a loan-to-value ratio (LVR) of 90% or below on principal and interest repayments (P&I).

Owner occupiers and investors across Australia are eligible for the 6.04% p.a. capped loan.

NICU Credit Manager Wayne Hoppe said the product provides customers the best of both worlds.

“Your interest remains variable, but it is guaranteed not to rise above a set interest rate for a three year period,” Mr Hoppe said.

“If the cash reference rate reduces, then the interest on the Capped Home Loan also reduces to reflect our Dream Home Loan variable interest rate.

“There are also no break costs if your circumstances change.”

How does a capped-rate home loan compare to a fixed rate?

A fixed-rate home loan gives you the option to lock in or ‘fix’ your interest rate for a set period of time - typically between one and five years. During that set period, the interest rate will not change, even if rates go up or down.

While you are protected if interest rates rise, you are unable to benefit from rate cuts.

By contrast, the interest rate on a capped-rate loan can drop. If the cash rate reduces, so too does your home loan interest rate.

Additionally, with a capped home loan, you have the option to make additional repayments, unlike a fixed-rate loan which typically does not offer flexible features like this.

Before applying for a home loan, ensure you assess your personal and financial circumstances to find the right fit for you.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by freepik

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia