.jpg)

Before a bank or home lender agrees to lend you money, it will ensure you meet its lending criteria and are in a solid position to take on the ongoing commitment of regular mortgage payments. Yet sometimes life happens, things change, and your financial position takes a hit.

There are many reasons borrowers may not be able to meet their scheduled mortgage repayments - job loss, relationship breakdown, mounting debts, sickness. So, what do you do if it happens to you?

What is a mortgage default?

First up, let’s be clear on what a mortgage default is. A default occurs when a borrower misses a loan repayment and fails to correct the issue quickly. Lenders have different definitions of what constitutes a default, but many will consider a mortgage to be in default if a repayment is overdue by 90 days.

Once you fall behind on a payment, many lenders will send you a default notice on the day the repayment becomes overdue, but some may wait until your repayment is 90 days late. When a default notice is issued, you generally have 30 days to pay the amount outstanding, including any regular repayments that fell due during that time.

It’s worth noting that although lenders may apply a 90-day tolerance, some credit agencies will record a default on a credit report when the repayment is 60 days overdue. There are some rules around this including that the lender must have issued notices to the borrower according to set time frames.

Once a mortgage default has been recorded on your credit history, it will remain there for five years although if a payment is eventually forthcoming, your file will be updated to show this.

Default & arrears: What’s the difference?

You might often see the words ‘arrears’ and ‘default’ used interchangeably, but there’s an important difference between them. Arrears refers to a loan being behind in payments at any point. Most lenders offer a one to two-week grace period once you miss a payment. This means any payment made during this period is still considered to be on time. After this, you are considered to be behind on your repayments and your lender will class you as being in arrears.

There are any number of reasons why someone may fall into arrears. They might have lost their job, fallen ill, or interest rates may have increased to a point where they can’t keep up with higher variable rate repayments.

After some time in arrears (it will be different for different lenders), the lender will send out a ‘notice of default’ which gives you 30 days to catch up on your repayments schedule. Lenders are restricted by law from requiring payment within a shorter period. Some lenders may send out a notice of default immediately after a repayment is missed, but most lenders won’t take this action until you reach the 90-day mark.

Mortgage stress and mortgage defaults

Another term often used in conjunction with arrears and defaults is mortgage stress. Mortgage stress occurs when a household finds it difficult to meet home loan repayments and cover other ongoing bills and expenses. The common definition of mortgage stress is when a household is spending more than 30% of its gross (pre-tax) income on mortgage repayments.

Not only does mortgage stress affect financial health, but it can also lead to detrimental effects on mental and physical health. If mortgage stress continues for an extended period of time, ultimately it can lead to home loan arrears and then mortgage default.

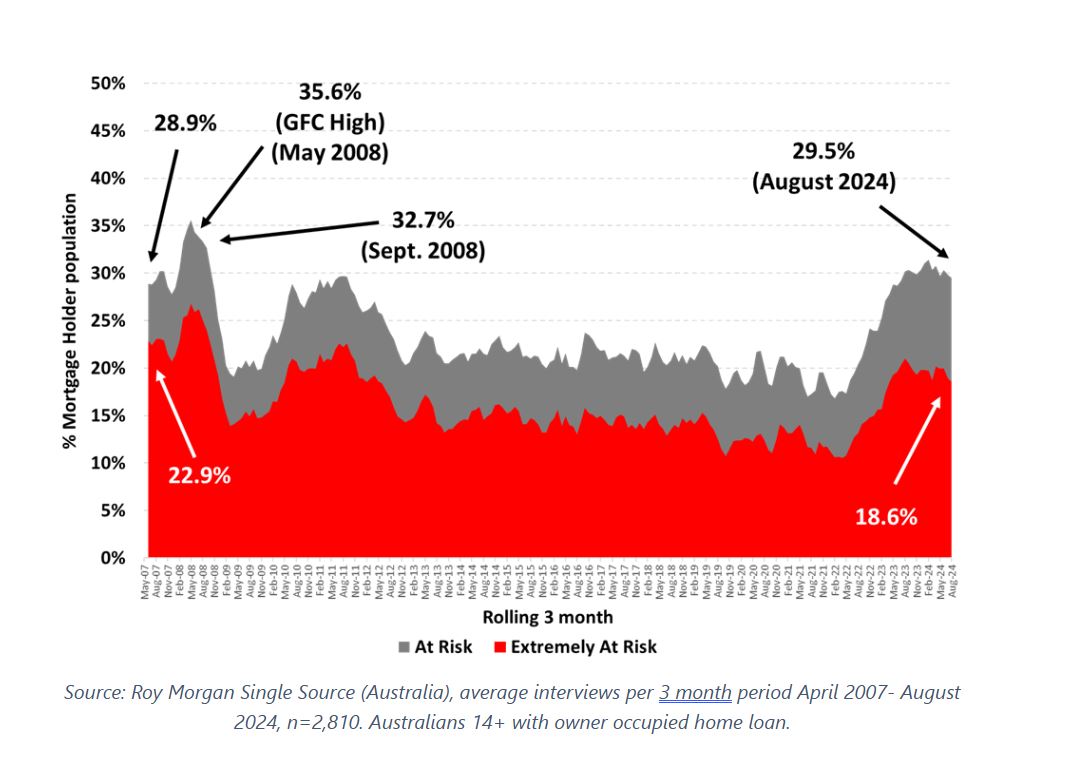

The latest mortgage stress statistics captured by Roy Morgan (as at September 2024) found more than 1.659 million Australian mortgage holders - or 29.5% - were at risk of mortgage stress over the three months to August 2024. The figure had dropped slightly over the previous period, attributed to the introduction of the stage three tax cuts and federal and state government energy rebates coming into effect in July 2024.

A record high 35.6% of mortgage holders in mortgage stress was recorded in mid-2008, coinciding with the Global Financial Crisis. The recent history of mortgage stress in Australia is illustrated in the graph below:

What happens when you default on your mortgage?

There are generally some fees that come with missing a mortgage payment, which can cost as much as $200 depending on the lender. Aside from being slapped with a late fee, the interest payable on your loan will also increase as you’ll have to make up the amount accrued because of those late payments.

A mortgage default will also be recorded on your credit report which can negatively impact your credit rating and significantly hamper your borrowing capability in the future. This can work against you if you decide to refinance your home loan or access other forms of credit.

See also: Can I refinance my home loan with bad credit?

By far the worst consequence of mortgage default is losing the roof over your head. If you fail to pay your overdue repayment within 30 days after the notice of default, your lender has the right to repossess the property and sell it in order to recover the debt. However, there are some steps you can take well before this happens.

Steps to take if you default on your mortgage

If you’re in danger of defaulting on your mortgage, or are just struggling to meet your repayments, you have a number of options. As with most financial matters, it’s better to take action as early as possible.

-

Contact your lender: Your first step should always be to go straight to your lender and inform them of your financial situation. Banks and lenders are required by law to have specialist financial hardship teams that can make short-term variations to your loan designed to cover a few months until normal payments can resume. If your situation is more dire than that, they can also assist you to come up with a longer-term plan. A long-term paying customer is worth far more to them than losing you off their lending book.

-

Reduce mortgage repayments back to the bare minimum: It may be possible to reduce your repayment amount or change the frequency of payments. You could do this by switching to interest only repayments until you get back on your feet. Your best move is to contact your lender to discuss the options open to you.

-

Access excess funds in the home loan: If your mortgage has an offset account or a redraw facility, you can use these extra funds to cover repayments for as long as they last.

-

Restructure your mortgage: Other options could include shifting your loan from a variable to a fixed rate or switching to a split variable/fixed rate which can effectively lower your repayments.

-

Refinance with a new lender: Another option could be to refinance your loan with another lender. Bear in mind, there are generally fees and charges associated with refinancing with another lender. There could also be break fees charged by your bank if you want to swap lenders. You need to consider all possible costs, as well as any benefits of refinancing, before making a decision. Our Cost of Refinancing Calculator can help with your considerations.

-

Downsizing: This might not be an easy decision to make, particularly if you’re attached to your home, but it might be the right one for your financial position. Moving to a cheaper home could free up hundreds of extra dollars each month thanks to lower home loan repayments. It’s also a far better outcome for you to sell your home yourself than have your lender sell it as a repossessed property.

Seeking help before a default

The Financial Rights Legal Centre’s sample letter generator can help you write a letter to send to your lender about your difficulty in meeting a home loan repayment. The lender must legally inform you of its response to your hardship request within 21 days. If it decides to reject your request, it must give you a written reason why, and if you aren’t happy with their rejection:

-

The lender must take it to its own internal dispute resolution team; then

-

You can contact the Australian Financial Complaints Authority (AFCA) to make a complaint and get a free and independent dispute resolution

During this time, you can also speak to a financial counsellor by calling the National Debt Helpline on 1800 007 007. The service is funded by the federal government and the state governments of Victoria and New South Wales and operates seven days a week.

How to avoid defaulting

Financial positions shift every day - such is life. Defaulting on your home loan may be unavoidable in some financial circumstances, yet there are several things you can do protect yourself against it happening.

-

Build up an emergency savings buffer beforehand: You should always aim to have around 3-6 months' worth of expenses set aside as an emergency savings buffer to call on when necessary. If you start to fall behind on mortgage repayments, you can draw on these savings as a safety net.

-

Don’t borrow outside your means: Simply put, the more expensive the home, the bigger your repayments will be. So, while the great Australian dream of owning a house and acreage has grand appeal, consider whether you can afford to meet the repayments on such a large purchase or whether you’re better off buying something more modest and working up to buying your dream home down the track.

-

Obtain a lower home loan interest rate: Besides buying an affordable home, arguably the most important thing you can do is to secure a home loan with a low interest rate. Even a minor difference in rates can save you hundreds to thousands of dollars each year. If you’re looking to refinance, the table below features home loans with some of the lowest interest rates on the market.

Lender Home Loan Interest Rate Comparison Rate* Monthly Repayment Repayment type Rate Type Offset Redraw Ongoing Fees Upfront Fees Max LVR Lump Sum Repayment Extra Repayments Split Loan Option Tags Features Link Compare Promoted Product Disclosure 5.54% p.a.5.58% p.a.$2,852Principal & InterestVariable$0$53090%- Available for purchase or refinance, min 10% deposit needed to qualify.

- No application, ongoing monthly or annual fees.

- Quick and easy online application process.

Promoted Disclosure 5.49% p.a.5.40% p.a.$2,836Principal & InterestVariable$0$080%- No application or ongoing fees. Annual rate discount

- Unlimited redraws & additional repayments. LVR <80%

- A low-rate variable home loan from a 100% online lender. Backed by the Commonwealth Bank.

Promoted Disclosure 5.64% p.a.5.89% p.a.$2,883Principal & InterestVariable$250$25060%- Easy application. Fast approval. 100% offset.

- Unlimited additional repayments free of charge.

- Redraw available - Access additional payments.

Promoted Disclosure 5.64% p.a.5.89% p.a.$2,883Principal & InterestVariable$248$35060%- Check your eligibility in as little as one minute

Disclosure Important Information and Comparison Rate WarningImportant Information and Comparison Rate Warning -

Don’t be afraid to seek help: The worst thing you can do is not do anything. Contact your lender, speak to a financial counsellor, and let your family or close friends know you are experiencing financial difficulty. As the old adage goes, a problem shared can be a problem halved. Allow others to help you come up with a solution.

")

Lender steps when you default

Now that we’ve covered what you can do in default situations, let’s consider what your lender may do. Selling your home to recover the debt is generally the last step a lender will take. In most cases when your loan first falls into arrears, they will contact you multiple times, send you the required default notices, and refer you to their financial hardship teams. There are a lot of safety nets before you lose your home so take advantage of them.

Usually, when you’re in arrears or are about to default on your mortgage, the lender will take the following steps:

-

Notify you of a missed or late repayment (although some lenders may issue you a default notice at this time).

-

Provide information and assistance regarding financial hardship and inform you of how to get in touch with their financial hardship team.

-

After 90 days of more of an overdue payment, they will issue a notice of default giving you 30 days to repay the overdue component.

-

If this isn’t paid within 30 days, the lender can serve you with a ‘statement of claim’ to begin legal proceedings against you.

-

You have a set number of days (this differs in each state and territory) to file a defence or lodge a dispute with a dispute resolution scheme.

-

If you do nothing, the lender can take action to repossess your home.

-

Once a lender gets a court order to repossess your home, they will send you a Notice to Vacate or a Sheriff’s letter asking you to move out of the home.

-

Even if your lender takes possession of your home, this does not release you from the obligation to repay the loan. Your lender may take further legal action to sell your home to recover any outstanding balance. If this doesn’t cover the cost of the loan, your lender may also make a claim to sell any other assets you have.

If you find yourself facing this situation and you want to be aware of what your rights are when a lender tries to repossess your home, you can contact the Consumer Action Law Centre or the federal government’s dedicated financial information service for free advice.

Savings.com.au’s two cents

Defaulting on your home loan is never a good thing, but sometimes it can’t be avoided. There are steps you can take before defaulting on your loan. There are also many more you can take after you default. The most important thing is that you take action as soon as you can. Your lender would much prefer to make arrangements to keep you as a paying customer on their lending book than lose you as a customer.

The best thing you can do is communicate with your lender as soon as you foresee yourself getting into financial difficulty and work with them to find a solution that best suits your circumstances. If you’re not happy with your lender’s response, you have some legal recourse which may help you come up with a better solution. Seek professional help by reaching out to free services that are there to provide advice and get you through such scenarios.

Default and eviction can be highly stressful, and if you’re experiencing financial or emotional distress because of it, you can contact:

-

Services Australia’s Crisis and other help service

-

Lifeline on 13 11 14

-

National Debt Helpline on 1800 007 007

Should you need it, you may also be able to access free legal aid via the National Association of Community Legal Centres website.

Article originally published September 2020 by William Jolly. Last updated 1 November 2024.

Image by Vitaly Gariev via Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Dominic Beattie

Dominic Beattie

Jacob Cocciolone

Jacob Cocciolone