The report from the Australian Securities and Investments Commission (ASIC) found one in five consumers had missed buy now, pay later (BNPL) payments, from providers like AfterPay, Zip, and Humm.

In the 2018/19 financial year, over 1.1 million transactions incurred multiple missed payment fees, which represents 45% of all transactions that incurred missed payment fees.

In the same period, missed payment fee revenue for all BNPL providers in the report totalled over $43 million, a growth of 38% compared to the previous financial year.

Need somewhere to store cash and earn interest? The table below features savings accounts with some of the highest non-introductory and introductory interest rates on the market.

- Bonus variable rate for the first 4 months on balances up to $250k and high variable ongoing rates.

- No fees and no monthly requirements to earn interest.

- Easily open an account online in 3 minutes.

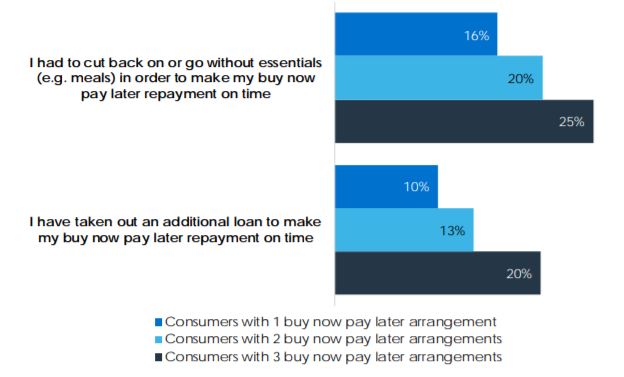

In the last 12 months, 20% of consumers surveyed by ASIC said they cut back on or went without essentials like meals in order to make BNPL payments on time.

Of this group, 49% were aged between 18 to 29, 50% had also missed a BNPL payment, and 32% also had a small and/or medium credit contract.

ASIC also found 15% of consumers surveyed said they had taken out an additional loan to make payments.

Of these, 50% were aged between 18 to 29, 68% had also missed a BNPL payment, and 44% also had a small and/or medium credit contract.

ASIC said these consequences were more prevalent among consumers who used multiple BNPL arrangements.

Source: ASIC

One in five consumers surveyed also reported they had missed or were late on paying other bills in order to make BNPL payments on time.

This included missing payments like household bills (44%), credit card payments (32%), and home mortgage payments (22%).

Gerard Brody, CEO of Consumer Action said the report's findings were concerning and called for greater regulation in the sector.

"It’s alarming if people are prioritising buy now pay later debts over essentials, or paying off other interest-charging loans," Mr Brody said.

"The best way to address this and limit the harm is to apply responsible lending obligations and other credit laws to the buy now pay later sector.”

BNPL sector posts enormous growth

ASIC reviewed AfterPay, Zip, Humm, BrightePay, Openpay, and Payright, and found there were 6.1 million accounts approved combined on the platforms, an increase of 38% from the 2017-18 financial year.

This represents up to 30% of the Australian adult population, although multiple accounts can be held by the same person.

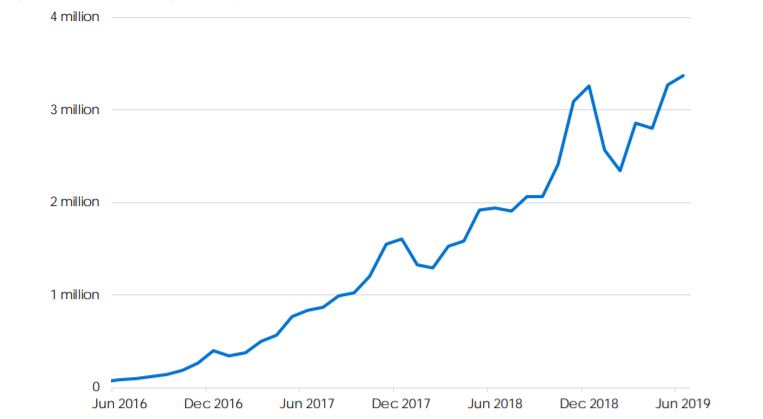

The number of BNPL transactions increased from 16.8 million in the 2017-18 financial year to 32.0 million in the financial year 2018/19, representing an increase of 90%.

Number of BNPL transactions June 2016 - June 2019

Source: ASIC

The total value of these transactions increased by 79%, from $3.1 billion in the 2017/18 financial year to $5.6 billion in the 2018/19 financial year.

Afterpay continued to have a stranglehold on the Australian BNPL market, accounting for 73% of that total value of transactions.

The provider hit back at ASIC and said despite having this lion's share of the market, Afterpay only represented 27% of BNPL consumer debt.

"Customers are immediately suspended from using Afterpay if they miss a single instalment payment," Afterpay said in a statement.

"For customers who find themselves in trouble, Afterpay offers a generous and accessible hardship program where flexible payment timelines with no additional fees or cost can be agreed upon."

But Mr Brody said there was a discrepancy in the reporting of hardship numbers by BNPL providers.

"Also, the industry is either ill-equipped, or not sufficiently motivated, to identify and assist those in hardship," he said.

"BNPL providers have said that no more than 1% of their users have been in financial hardship during COVID-19 but the data in this report confirms that the real figure is likely much higher, and industry players are either underreporting or not actually able to identify hardship."

Total revenue from BNPL arrangements across the six providers grew by 50%, from $266 million in the 2017/18 financial year to $398 million in the 2018/19 financial year.

Revenue sources include merchant fees, missed payment fees, and other consumer fees (e.g. establishment fees, account-keeping fees).

BNPL's explosive growth has come at the cost of credit card popularity.

The value of personal credit card transactions increased by 3.6%, from $258.1 billion to $267.3 billion, in the 2015/16 financial year.

From the 2017–18 financial year to the 2018–19 financial year, it grew at a much slower rate of 0.3%, from $273.7 billion to $274.5 billion.

BNPL users more likely to incur credit card interest charges

ASIC found between 66% and 73% of BNPL users incurred interest charges on their credit cards for all months between October 2019 and January 2019.

In the same period, only 42% to 46% of other credit card users incurred an interest charge on their credit card.

Additionally, between 38% and 43% of BNPL credit card users used over 90% of their allocated credit limit on their credit cards for each month between October 2018 and January 2019.

In the same period, only 16% to 18% of other credit card users did the same.

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Emma Duffy

Emma Duffy

William Jolly

William Jolly