But unless you've just won $50,000 on Millionaire Hot Seat like a certain ex-boyfriend who shall remain nameless, you're going to have to save up for your house deposit all by yourself.

We've put together a guide on how to save up for a house deposit that includes no mention of smashed avocado (except for that one. Sorry).

How much deposit do you need for a house?

You normally need to put down a deposit that is equal to at least 5% of the value of the home to buy a house. For traditional banks, that's usually the smallest deposit they will entertain, though many lenders will require significantly more than that.

We've probably all heard that a 20% deposit (20% of the value of the property) is the sweet spot. That's because a 20% deposit usually means you won't be hit with the cost of lenders mortgage insurance (LMI).

LMI is a one-off payment that covers the mortgage lender against any loss that may occur in the event the borrower is unable to make their loan repayments (a default on the loan). If a borrower defaults on their mortgage, the lender can recover what is owed to them by repossessing the property the home loan is tied to. But if the value of the property has fallen, the lender can suffer a loss. This is the risk LMI covers.

Lenders typically exempt borrowers from having to pay LMI if the deposit is at least 20% of the property's value or sale price. That's because a 20% deposit is usually considered to be a big enough buffer to protect lenders from a drop in the value of the property, which gives them a strong chance of recouping the amount that's owed to them if the borrower defaults on the loan. Also, lenders may perceive borrowers who have deposits over 20% to be more responsible, thus less likely to default on the loan.

How much is Lenders Mortgage Insurance?

LMI can be very expensive. For example, if you buy a $500,000 home with a 5% deposit ($25,000), you'll face an estimated LMI cost of $21,423 (according to Savings.com.au's Lenders Mortgage Insurance Calculator).

However, there can be times where it may be worth paying for LMI. If property values rise over the time it takes you to come up with a 20% deposit, you'd pay more on the purchase price than you would have if you'd snapped up a house back when you only had a 5% deposit. Because prices have risen, what would have been a healthy 20% deposit when you started saving may now only be worth 15%.

Stamp duty

There are other costs to factor into the deposit, such as stamp duty. Stamp duty is the tax on the sale of the property and covers the costs of changing the title of the property and ownership details.

If you're a first home buyer, there are stamp duty discounts available in most states and territories. Depending on the purchase price of the property and which state you're buying in, you may even be exempt from stamp duty.

How long does it take to save for a house deposit?

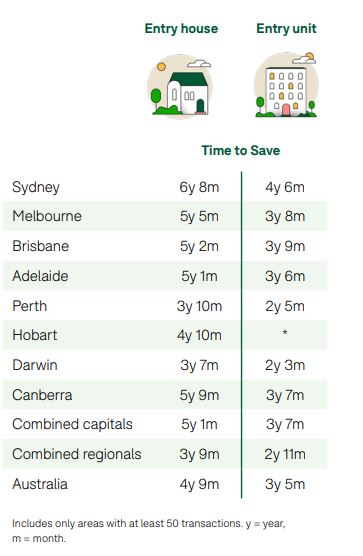

How long it takes to save up for a house deposit depends on a number of factors: your income, your expenses, and where you want to buy. Depending on where you live in Australia, saving for a house deposit can take anywhere from a few years to nearly a decade. However, this doesn't take into account rising house prices, which is one of the biggest challenges facing first home buyers.

Below is recent data on the estimated time it will take for a couple aged 25-34 to save a 20% deposit on an entry level home (both houses and units):

Source: Domain First-Home Buyer Report 2024

And here is a guide to the price of entry-level homes (20th percentile value) in each Australian city and nationally, as at January 2024:

| Region | Dwelling | Houses | Units |

| ACT | $626,958 | $786,179 | $463,604 |

| Adelaide | $536,622 | $610,855 | $401,884 |

| Brisbane | $576,786 | $652,657 | $449,224 |

| Darwin | $501,520 | $473,261 | $284,850 |

| Hobart | $509,030 | $537,514 | $445,819 |

| Melbourne | $566,868 | $704,828 | $452,679 |

| Perth | $516,957 | $559,560 | $358,631 |

| Sydney | $765,209 | $955,978 | $600,463 |

| Combined capitals | $588,184 | $676,543 | $489,603 |

| National (including regional areas) | $511,992 | $556,650 | $442,698 |

Source: CoreLogic 2024

What can I use as a deposit?

Now that you know how much you need to save and how long it might take you to reach that goal, how much do you actually have to save? Can you access funds from other sources? Let's check some options.

Can I use my super as a deposit?

The short answer to this one is: not exactly.

While you can't really raid your superannuation fund for a house deposit, you can leverage your super through the First Home Super Saver Scheme (FHSSS).

Under the scheme, first home savers can make voluntary concessional (taxed at a discounted rate of 15%) and non-concessional (already taxed at your marginal rate) contributions into their super funds which can be withdrawn later for a house deposit.

Can I use my inheritance or a gift as a deposit?

When it comes to taking out a home loan, many lenders prefer to see what are called 'genuine savings' or money that you have saved yourself over a period of time - usually between three to six months. This can demonstrate your ability to manage money and could indicate you'll be a responsible borrower. However, you can have gifts or inheritances approved as genuine savings if you have a letter from the gift giver/executor in some situations.

The amount of money will also need to meet certain requirements if you want to avoid the genuine savings rule. Most lenders will require a 20% deposit to avoid the genuine savings rule. Very few lenders will accept a 10% deposit without the need to confirm genuine savings.

The same rule applies to inheritance money. An inheritance can be used as a house deposit, but you'll need a 10-20% deposit to bypass the genuine savings rule.

Can I use the First Home Owners Grant as a deposit?

If you're a first home buyer and you're accessing the First Home Owners Grant (FHOG), you can technically use this to form part of your deposit if you're buying or building a new home.

As the name suggests, these state and territory government grants act as an incentive for first home buyers to purchase their first property. The amount of financial assistance varies between states, which means you'll need to research what applies to where you're purchasing. One condition many of the states have in common is that the grants only apply to the purchase of newly built homes - or properties that have never been occupied before - or the construction of a new property by the first-time buyer.

The FHOG alone often isn't enough to make up a full house deposit. At the time of writing, the maximum grant available is $30,000 in Queensland. In other states, it's between $10,000 and $15,000.

Can I get a 100% mortgage?

Since the Global Financial Crisis, true 100% home loans are a thing of the past. The only real way to borrow 100% of the property's value these days is with the help of a guarantor which some lenders allow. We'll talk more about using a guarantor later.

How do I save the money for a deposit?

This is where the hard work begins. To save for a home deposit, these are the three main steps to take, which we'll break down in more detail below.

- Look at what you're actually spending

- Make a budget

- Maximise your savings

1. Look at what you're spending

You spend a lot of time and energy earning it, but do you actually know where you spend your hard-earned cash? Tracking your spending is key when you've got big savings goals to kick, like a house deposit.

Tallying your income against your expenses, credit repayments, and savings can help you understand the areas where you can cut back in order to save more money. Saving a minimum of 20% of a property's value while still making regular rental and bill payments can be a challenge, but knowing where your money is going and working out where you can cut corners is a good place to start.

There are a few spending tracker apps you can use to track where your money is going. The great thing about tracking where every dollar is going is that you can identify some easy wins. You may have automatic payments going out for services you've completely forgotten about, like a gym membership or TV streaming service you never use. These are pretty simple things to trim from your spending, but you may not even be aware of them until you start tracking.

Once you know where all your money is going, you should have a pretty good idea of how much extra money you have each month to devote to your savings instead, and what expenditures you can offload to free up even more money.

Double down on debt

If you have any credit card, buy now pay later, or personal loan debt, you'll want to eliminate this before you approach a lender. Devoting funds elsewhere when you're trying to save up for a house deposit may seem counterintuitive, but it can be important. Any debt you carry will decrease your borrowing capacity when you apply for a home loan. Lenders may also be less willing to give you a home loan if you have too many debts.

Keep in mind, the interest you're paying on your debt is eating into your ability to save for a house deposit because it's compounding (growing bigger over time). The sooner you can attack your debts, the sooner you'll have more money to devote to your savings goal instead.

2. Make a budget

In most cases, a good budget should be realistic and have wiggle room. But when you have a pretty substantial savings goal, your budget will need to be more aggressive if you want to meet that goal quickly. This means you'll have to cut non-essential spending and be prepared to live frugally while you save.

The real trick here is to be brutally honest with yourself about how you spend your money. If you pretend you don't buy a bottle of wine every Friday night and omit that from your budget to make yourself feel better, you're lying to yourself to the tune of about $1,040 bucks a year.

Some people use the 50/30/20 rule for budgeting (50% for necessities, 30% for wants, 20% for saving). This is normally a pretty ideal budgeting strategy. But because you're saving for a house deposit, you may want to allocate more than 20% of your income towards savings. There may be areas in the 30% 'wants' section you can cut, such as spending less money on clothes or cooking at home instead of dining out and buying takeaways. You may also need to trim items in 50% necessities budget too, such as spending less on rent or reducing your bills.

3. Maximise your savings

As soon as your pay hits your bank account, you want to immediately siphon off the largest possible chunk you can afford into an untouchable high interest savings account.

To save for a deposit faster, there are a few options you may want to consider:

Move back home/live with flatmates/downgrade

Trying to save for a house deposit while paying ludicrous amounts of rent every week is difficult. While rent and bills are often non-negotiable, there are ways to trim costs. If your parents haven't renovated your childhood bedroom into a home gym yet, you might want to just suck it up and move back home while you save. Not only will you not have to contend with the significant expense of rent, there's a good chance your parents will look after many of your grocery expenses too. This frees up a significant chunk of cash to pop straight into your savings account.

If the thought of living with your parents again is just way too depressing (or it's not an option for you), there are other ways you can cut down on the amount you spend on rent each week. If you've got a spare bedroom, advertise for a flatmate to split the cost. Or settle for living in a crappy rental share house with six other people where the rent is cheap as chips.

Work hard for the money

It's important to decrease your expenses when you're saving for a house deposit, but have you considered ways to boost your income too?

If you've been at your job for a few years and have been performing strongly and adding value, you may want to consider asking for a raise. If that's not an option, there are still ways to make a little extra income. Enter the side hustle.

These days there are heaps of ways you can pull in some extra cash. Driving for Uber, pet sitting, doing jobs on Airtasker, or renting out your car space. The options are endless.

Netflix and... save?

It's tough to save, especially when you love all three of your streaming services. We believe in 'treat yo self' moments as much as the next person (we're not bloody monsters) but it's probably a good idea to pick one favourite and cancel the rest, depositing the savings straight into your house deposit fund.

Use a high interest savings account and automate your savings

When it comes to storing your hard-earned savings, an untouchable savings account earning the highest interest rate possible is a good spot to stash it. Once it's established, immediately transfer the biggest possible chunk from your paycheque into your house deposit fund. Make it easy for yourself by setting up an automatic transfer with your bank. That way, the money goes straight into your savings without you even having to think about it.

As far as you're concerned, that money doesn't even exist. Even when you're feeling crappy and there's a shoe sale on at Nine West, you do not touch your house deposit fund. It's the Holy Grail of your financial future.

Consider investing

You don't necessarily need to store your house deposit fund into a straightforward savings account. Even in the current high interest rate environment, house prices in many areas are increasing much faster than what you can earn in interest.

Fortunately, there are a few things you can do. You may want to invest in an asset class that's likely to see a stronger return than your savings account, such as shares or even property. That's right, you may want to consider putting your money into the asset class you want to buy.

You don't have to buy property to invest in the property market. There are funds that invest in real estate, allowing investors to buy shares and get returns based on the performance of the properties in the trust. Real Estate Investment Trusts (REITs) are an example of this type of fund. You need to do your homework before you invest your hard-earned cash, however. Remember, savings accounts in Australia are risk-free while the share market isn't.

Sell unused items

Getting rid of your unwanted belongings and furniture by selling them online can contribute a healthy amount towards your house deposit fund. It also gives you a clean slate for when you move into your new home.

Use public transport

Taking public transport or riding your bike to work can help your hip pocket (as well as your carbon footprint!). If you're feeling particularly thrifty, you may want to consider selling your car and storing the proceeds into a high interest savings account. Selling your car can immediately contribute thousands towards your house deposit.

Bank that bonus money

It might be tempting to spend your tax refund on a holiday or a new dress from The Iconic, but if buying a house is your goal then you just can't. Sorry.

Bank your tax refund straight into your high interest savings account. The same applies if you receive a pay rise. Invest the difference between your old pay and the new into your savings as soon as you get paid. It's easy to fall into the trap of absorbing any increases in pay (what's known as lifestyle creep) but if you could get by just fine on your old paycheque, stick to the same budget and invest the difference.

What help is available?

When you're saving for a house deposit, the road ahead can look very long. But there's help available.

First home owner grants

Many states and territories offer help to eligible first home buyers in the form of a grant. It's a one-off payment which is usually paid at the time of settlement to your home lender and applied directly to your home loan.

First Home Super Saver Scheme

Under the First Home Super Saver Scheme, first home savers can make voluntary concessional (taxed at a discounted rate of 15%) and non-concessional (already taxed at your marginal rate) contributions into their super fund which can be later withdrawn for a deposit on a first home.

The scheme is undergoing some technical changes that take effect from 20 September 2024, designed to improve its operation and allow greater flexibility.

Keystart and Homestart

If you live in South Australia or Western Australia, there are a few options that may help give you a leg up on the housing ladder.

Keystart

Keystart is an initiative sponsored by the Western Australian government, providing a number of low deposit solutions for WA home buyers. There are low-deposit home loans specific to the Perth metropolitan area that facilitate loans with deposits as low as 2%. There are also home loans aimed towards buyers in regional areas, single parents, indigenous Australians, and those on the disability pension. The loans are income-tested, so head to Keystart's website to see if you're eligible.

HomeStart

HomeStart offers low-deposit home loans (as low as 2%) to eligible South Australians and does not charge Lenders Mortgage Insurance. There are also options designed to boost buyers' borrowing power through a shared equity scheme, lower interest rate loans, or interest and repayment-free periods of up to seven years. The loans are income-tested, so head to Homestart's website to find out if you're eligible.

Stamp duty concessions

As we've already mentioned, stamp duty is a state and territory government tax on the sale of property, taking in the cost of changing the title of the property and ownership details. It can add tens of thousands of dollars to the cost of a home loan, so you need to take it into account when saving for a house deposit.

Fortunately, most states and territories offer stamp duty discounts for first home buyers. Depending on the purchase price of the property and where you're buying, you may even be exempt from paying any stamp duty at all.

Can I buy a house with no deposit?

If you've read this far and are ready to throw in the towel, don't give up on your dreams of home ownership just yet. There are other ways into the property market -- it just means getting a little more creative.

Rentvesting

Rentvesting is the practice of living in a rental property at the same time as renting out an investment property you own. Rentvesters typically rent property in the area they want to live in (but can't afford to buy) and buy property where they can afford (but don't want to live) and rent it out as an investment property.

You'll still have to save for a deposit, but it could be significantly smaller.

The idea behind rentvesting is that you can use your investment to generate cash flow, and eventually sell your property for a capital gain. If your capital gain is strong enough, you may be able to use that as the deposit for the property you really want to live in. Let's consider the case study below:

Case Study: Maria

Maria lives in Sydney where she rents an apartment for $350 a week with one other flatmate. She wants to buy an $850,000 unit and needs to save a 20% deposit of $170,000 - a pretty daunting amount of money to come up with.

She thinks about investing in Hobart where prices are considerably lower. The median unit price in Hobart is a much more affordable $520,000. For a 20% deposit, Maria needs to save $104,000, while a 5% deposit is a much more manageable $26,000. Saving $26,000 is a lot less scary than saving $170,000.

Buying in Hobart allows Maria to enter the property market at a more affordable level, although rentvestors should always do their sums first. Rental income from the Hobart unit may not cover Maria's investor loan (which generally attracts a higher interest rate than an owner occupier loan). Although Maria may receive some tax benefit from negative gearing on the Hobart unit, she must still ensure she is able to service the loan and continue to pay rent in Sydney.

Guarantor

Using a guarantor is akin to being approved for a no deposit home loan where your parents or another immediate family member offers the equity in their property to secure the loan. Essentially, this means that instead of paying a deposit, your family member signs a contract stating they'll be responsible for your home loan if you default on it.

If you have someone in your life (typically your parents) willing to be your guarantor, you can potentially avoid a deposit altogether. You may even be able to avoid paying LMI completely as the size of the deposit is determined by the equity your family member is putting up.

Obviously, this option is one that should not be entered into lightly - for either party. If you default on the loan, your parents are the ones who'll pay for it. If they've put their home up as security for your loan, they could lose their house if you default. However, once you've made enough repayments to cover the amount they've guaranteed, they will be released from the contract. This may take some years, however.

Savings.com.au's two cents

Saving for a house deposit is hard work - and far more difficult if you're on one income or renting while you're trying to save. Sadly, data shows it's as tough as it's ever been, given home values have been outstripping income growth for some years now. But it's not impossible.

If you're serious about saving for a deposit, there are ways to get there sooner if you're willing to sacrifice. If a bigger deposit is out of your reach, there are options for you.

Let's be optimistic. Once you've got your house deposit saved and you've found a house you want to buy, here's what to do with it next.

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.54% p.a. | 5.58% p.a. | $2,852 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.49% p.a. | 5.40% p.a. | $2,836 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure | ||||||||||

5.64% p.a. | 5.89% p.a. | $2,883 | Principal & Interest | Variable | $248 | $350 | 60% |

| Disclosure |

")

Image by Lumina Images via Adobe Stock

Disclaimers

The entire market was not considered in selecting the above products. Rather, a cut-down portion of the market has been considered. Some providers' products may not be available in all states. To be considered, the product and rate must be clearly published on the product provider's web site. Savings.com.au, yourmortgage.com.au, yourinvestmentpropertymag.com.au, and Performance Drive are part of the Savings Media group. In the interests of full disclosure, the Savings Media Group are associated with the Firstmac Group. To read about how Savings Media Group manages potential conflicts of interest, along with how we get paid, please click through onto the web site links.

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Rachel Horan

Rachel Horan