The property market for 2021 has been raining cash with annual property price growth hitting levels not seen for more than 30 years.

Lockdowns across the nation didn't deter Australians from capitalising on the booming market, with sellers cashing in and buyers scrambling to purchase to avoid FOMO pushing the national housing market towards a median price of $1 million.

Corelogic reported in October the average annual property price growth rate reached 20.3% for the first nine months of 2021, 17.6% higher than the same period in 2020.

Sydney recorded the highest median growth across all capitals throughout the year, with Domain reporting the median increased by 30.4% or about $349,000 over the year to September.

This marks the strongest annual growth since Domain records began in 1993, with prices in half a dozen NSW regions surging at least $500,000.

2022: House prices to continue to grow at reduced pace

The 'Australia's Housing Rolling Over' report published on Thursday by ANZ senior economists Felicity Emmett and Adelaide Timbrell details low interest rates, strong fiscal support during the worst of the lockdowns and high savings all combined to drive house prices up strongly - a trend seen repeated around the world.

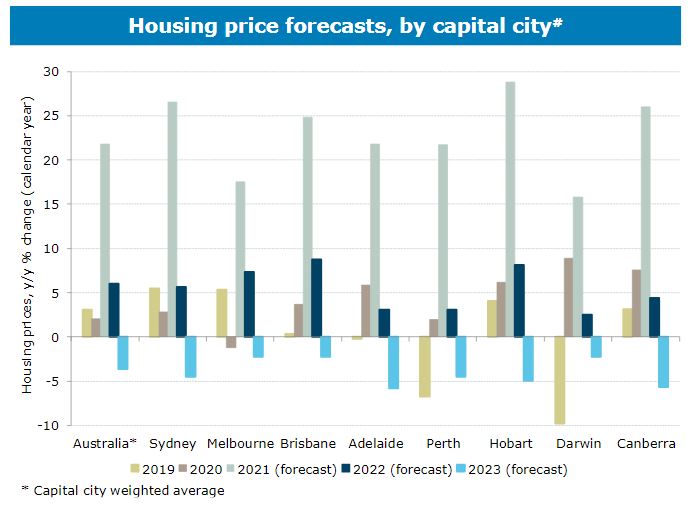

Bank economists tipped property prices to continue to grow in 2022, before interest rates and regulatory action stifle growth in 2023.

ANZ forecasts an average national growth in property prices of 6% in 2022, before falling 4% in 2023.

The strongest gains will be seen in Brisbane, with a 9% rise, Hobart, up by 8%, and Melbourne rising by 7%.

Sydney’s long surge will be moderate compared to 2021, up 6% next year, on ANZ’s outlook.

Source: ANZ

APRA, lenders watching after tightening screws

Following actions taken by the prudential regulator a month ago coupled with strengthen lending policies, the market has steadied throughout the fourth quarter, responding to financial conditions tightening.

ANZ's senior economists believe the market may continue to do more of APRA's work for it, particularly on the back of fixed interest rates rising,.

Buyers agent Michelle May believes the actions taken by APRA this year will contribute to a sharp decrease in lending among first home buyers with the market being 'out of reach' for them.

"Those first home buyers that are able to still get into the market will have to turn back to apartments - otherwise, they risk renting for the longer term as the disparity between apartment and house price increases have been significant," Ms May said.

ANZ's senior economists note the diminishing number of first home buyers entering the current market - hoping to 'ride out' the property boom paired with the unwinding of government schemes - has sparked the number of new home approvals to fall rapidly throughout 2021.

Interest rates hold the key

Affordability constraints and a better supply-demand balance may help to slow the market, yet interest rates will be critical to future price developments in the housing sector.

ANZ's economists believe the underlying cash rate will lift in mid-2023, forcing banks to raise their own interest rates and passing those costs on to consumers.

The Reserve Bank of Australia states it will only lift the rate from 0.10% once inflation sustainably hits its 2% to 3% target band, with that inflation driven by wage growth of at least 3%.

The ABS recorded inflation data of 2.1% in the September quarter, which banks have taken as a sign of the strengthening of the economy and as a result have shown no hesitancy in raising fixed interest rates.

Wages must increase in reaction to market

In the year to October, CoreLogic reports a 20% deposit on the median Australian dwelling value has increased by $25,417, to a total of $137,268.

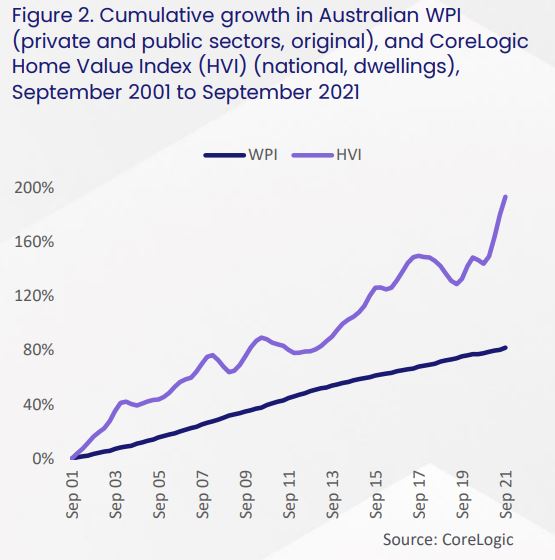

Over the same period, wages have increased just 2.2%, resulting in Australians facing increased difficulties to grow household savings to keep up with this kind of price increase.

Data published by CoreLogic details that while wages have increased 81.7% in the past 20 years, Australian home values have grown 193.1%.

For many Australians the high median house prices across the country when coupled with subdued wage growth means purchasing power is limited when it comes to mortgage serviceability over time.

This ultimately means that households cannot pay down their mortgage as easily or quickly.

CoreLogic's research director, Tim Lawless, said with housing values rising substantially faster than household incomes, raising a deposit has become more challenging for most cohorts of the market, especially first home buyers.

"Sydney is a prime example where the median house value is now over $1.4 million," Mr Lawless said.

"In order to raise a 20% deposit, the typical Sydney house buyer would need over $260,000."

ANZ's economists said the widening gap between wages growth and house price rises had made it extremely difficult for those who did not already own property to get into the market.

Image by R Architecture via Unsplash.

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harry O'Sullivan

Harry O'Sullivan

Bea Garcia

Bea Garcia

Denise Raward

Denise Raward

Brooke Cooper

Brooke Cooper

Rachel Horan

Rachel Horan