We substitute the stress of the financial burden we’re undertaking for decades to come, for the stress of juggling full-time uni, a job, a social life and sleep, with often less than desirable results.

Many of us don’t even look at the costs of the classes we’re undertaking at uni – instead, we’ll ignore these obtuse amounts until we actually make enough money to start our repayments (which is ages away… right?).

However, according to 2018 figures from the ABS, average weekly earnings for all employees in Australia (full-time, part-time and casual) are $1,225, which equates to $63,700 per year. At this average salary, you’d be required to put 4.5% of your annual income (over $2,800) towards a HECS debt repayment.

So should you be one of the lucky few to get a position in your field after graduating, chances are you’ll immediately begin paying off your HECS debt. So how does it all work?

What is a HECS-HELP debt?

Let’s work our way through the government jargon and abbreviations first:

HELP

- Is a Higher Education Loan Program that encompasses all the loans that you’ll find below

CSP

- Is a Commonwealth Supported Place

- Is a university or higher education institution where the government subsidies a portion of your fees

- Typically you will pay the rest, referred to as the ‘student contribution amount’, via a loan

- A CSP is essentially all public universities, and a small number of private ones

HECS-HELP

- HECS is a Higher Education Contribution Scheme

- You can only get a HECS loan if you are studying at a CSP

- Generally applies to public universities

FEE-HELP

- This loan covers tuition FEE’s, for those not studying at a CSP

- It generally applies to private universities and high vocational training

SA-HELP

- A Student Amenities is a loan that covers the student services and amenities fees (SSAF)

- Essentially all tertiary education institutes have these fees, which cover campus facilities such as career guidance and recreational activities

OS-HELP

- This loan applies to students at CSP’s who are looking to go Overseas for study purposes (exchange)

- You must be studying full time when you go overseas and also have completed one year of full-time study prior

- You also cannot be in your final semester of study.

The eligibility for these loans are fairly straightforward. You must be either:

- an Australian citizen,

- a New Zealand Special Category Visa (SCV) holder,

- or a permanent humanitarian visa holder

You must also:

- have a Tax File Number (TFN)

- be enrolled in your courses by your institutes’ census dates

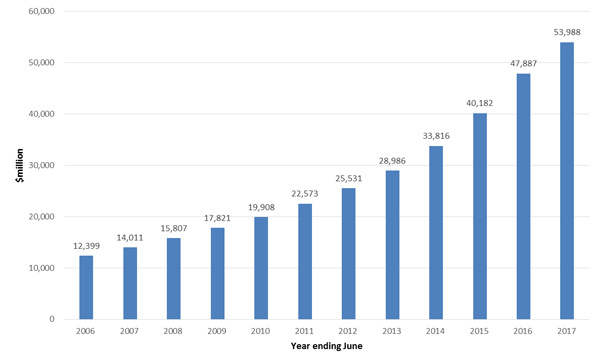

Once uni rolls around and census date for that semester has arrived, that’s it, your debt has begun, how exciting! You’re now one of the millions of people who owe the government billions (see below for the absurd figures).

Figure 1: Total amount of outstanding HELP debt 2005–06 to 2016–17 financial years ($m)

Source: ATO, Taxation Statistics 2015-16, published 27 April 2018

HECS interest rate

HECS-HELP loans are often referred to as the best debt you can have, as they don’t have a time limit on them and are 100% interest free.

Instead of interest, your debt is annually compounded by the national indexation rate. Confused? It simply means the debt is raised each year in line with the cost of living. Last year, the indexation rate was 1.9% – so if you earned $60,000 and if your debt was at $40,000 at the end of financial year, your repayments would be $2,400 and the indexation rate would cost you $760, leaving your debt at $38,360 after your first year of paying it off.

HECS repayment threshold & rates

By the end of your student life, you’ll have uploaded a photo onto social media of you in your graduation gown, ready to take on the world. What next? Use that degree to get a job.

If you land a position earning above a specific threshold ($51,957 at the time of writing), you’ll be required to begin repayments on your loan. The more you earn above that threshold, the higher your repayments will be.

The thresholds change every year, so make sure you check the ATO website for the most up-to-date information. Keep in mind that if you’re earning above the minimum repayment threshold while you’re still studying, you’ll still have to make repayments.

These are the repayment rates for the year to June 30, 2019.

| 2018-2019 Repayment Threshold | Repayment rate (%) |

|---|---|

| Below $51,957 | Nil |

| $51,957 – $57,729 | 2.0% |

| $57,730 – $64,306 | 4.0% |

| $64,307 – $70,881 | 4.5% |

| $70,882 – $74,607 | 5.0% |

| $74,608 – $80,197 | 5.5% |

| $80,198 – $86,855 | 6.0% |

| $86,856 – $91,425 | 6.5% |

| $91,426 – $100,613 | 7.0% |

| $100,614 – $107,213 | 7.5% |

| $107,214 and above | 8.0% |

* Data accurate as at 26th June 2019.

HECS-HELP and tax

When you do start working, you’ll have to notify your employer of your HECS-HELP debt through a tax declaration. From there, they’ll set aside additional tax from your pay to cover your estimated repayment. Although you’ll then have amounts coming out of your pay cycles, the compulsory repayment won’t happen until you lodge your tax return. Hopefully your deductions will be correct and that will be the end of it, but any incorrect deductions may result in you having to pay more, or potentially receiving a refund.

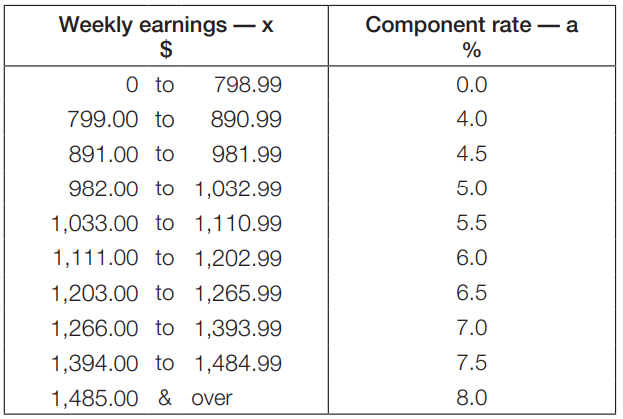

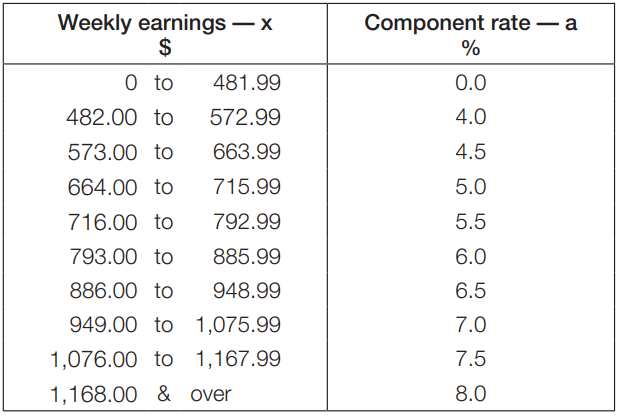

Below are two HECS tax tables to help you calculate the monthly withholding amount for your earnings:

If tax-free threshold is claimed

Source: ATO Schedule 13 Pay as you go (PAYG) withholding 2008

If no tax-free threshold is claimed

Source: ATO Schedule 13 Pay as you go (PAYG) withholding 2008

Moving overseas for work? Sorry, you’ll still have to pay off your HECS-HELP debt. This used to be a loophole that cost the government around $30 million in annual repayments, but was closed in 2016.

If you fall under the minimum $51,957 income bracket at any point or go bankrupt, your payments would cease.

God forbid you pass away, you needn’t stress from beyond the grave, your debt will be cancelled.

You can get any information on your loan, such as how much you owe, by logging in to your myGov account or by contacting the ATO.

Should you make voluntary payments?

In the past, people could get a 10% discount if they made a voluntary student debt repayment over $500, but the discount was removed in 2017.

It’s generally advised that you pay off your most expensive ‘bad debt’ first. Credit card debt and personal loans for a car or holiday fall under this category.

However, if you’re debt-free (excluding your HECS-HELP debt) upon graduating your study, making dents in that amount will likely be beneficial in the long run, especially if you are paying it off years in advance.

If you’re looking to break into the housing market, some years down the track, having a HECS-HELP loan could reduce the amount of money you’re eligible to borrow for a mortgage. This is one reason why some people choose to pay off their HECS-HELP debt earlier.

Voluntary payments can be made to the ATO via BPAY or via credit card.

Savings.com.au’s two cents

University can be expensive, but it can be one of the best financial investments to make in your future. Even though it can leave you with quite a large debt, tertiary qualifications should give you more opportunities in your career and potentially help you earn more money over the course of it.

Don’t go blindly into the abyss – research your courses thoroughly and understand the financial burden you will be taking on. University subjects are expensive – some can cost thousands of dollars each. That’s why it’s important to think about your HECS debt while you’re accruing it – not just while you’re paying it off.

Despite the high costs of study, pursuing a higher education can still be worth the debt. Giving yourself the best opportunity to earn a substantial, reliable income in your future far outweighs temporarily losing a little bit of your salary each week.

Upon completion of your degree, budget accordingly with your HECS-HELP loan incorporated, and plan for the future with it in mind.

Emma Duffy

Emma Duffy

Harry O'Sullivan

Harry O'Sullivan