According to the Clean Energy Finance Corporation (CEFC), modelling shows that electric vehicles could make up 90% of all cars on Australian roads by the year 2050 with $1.7 billion worth of investment.

While that’s relatively little in the grand scheme of things, electric vehicle use could be set to surge as early as 2021. According to The Australian Bureau of Statistics (ABS) Motor Vehicle Census data, electric vehicle registrations almost doubled in 2020 compared to 2019 (although they still represent a tiny percentage of overall cars).

‘Green’ cars are said to be the way of the future, and there are many advocates out there who say they are also cheaper to own over time. With this in mind, we’ve prepared a green vehicle guide, to help you figure out just how environmentally friendly your next set of wheels is, and whether it could save you money.

On this page:

What is a ‘green' car?

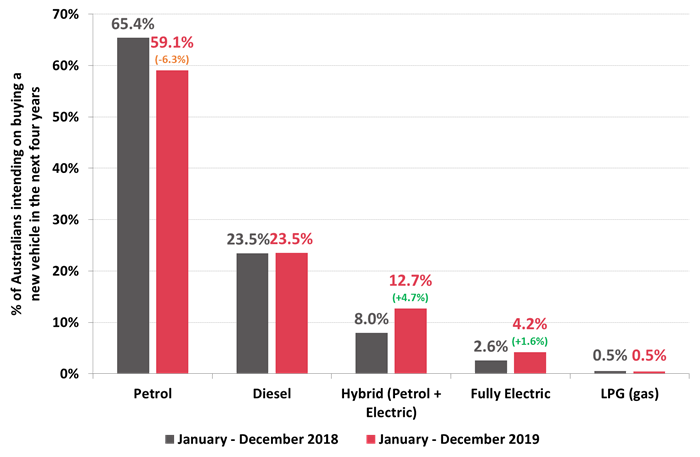

There’s often no set definition for what a green car is. Some might consider it to be a car that produces no emissions like electric cars that run on rechargeable batteries, or cars that produce very few emissions such as hybrid cars, which combine petrol and electric engines. These cars are becoming increasingly popular as of late: Roy Morgan Research found a 4.7% and 1.6% rise in the number of people intending to buy either a hybrid or electric vehicle respectively in 2020, compared to 2019, while fewer people intended to buy a petrol model.

Source: Roy Morgan

Other definitions extend the list to cars that simply produce ‘low carbon emissions’. There are already vehicle emissions standards for all cars sold in Australia, but green vehicles are ones that go beyond satisfying these standards, and they don’t necessarily have to be electric or hybrid models. They can use the various types of petrol, even diesel, depending on how environmentally-friendly they are (more on this later).

Green vehicle guide

A Federal Government initiative dating as far back as 2004, the Green Vehicle Guide (GVG), is an online comparison tool to help consumers search for and compare various vehicles based on their environmental performance. It mainly measures greenhouse gas emissions, primarily carbon dioxide (CO2), and displays how much of this carbon dioxide each vehicle emits in grams per kilometre (g/km).

On average, Australian cars emit 182 g/km of CO2, and the worst offender emits more than 370. There are some fully electric vehicles that emit zero CO2 (g/km), while others will emit below the average. As well as the CO2 (g/km), the Green Vehicle Guide provides information on the following:

-

The annual fuel cost: This can help you compare how much it might cost to fill up your car’s tank compared to other models, based on a set distance.

-

The average fuel consumption (L/100km): This can help you find the most fuel-efficient vehicle based on your needs.

-

The energy consumption and electric range: For electric or hybrid vehicles, this can help compare which car has a better range (distance) and which is the most energy-efficient.

-

The air pollution standard: Vehicles that score well on this produce lower levels of harmful pollutants, such as photochemical smog, hydrocarbons (HC) and oxides of nitrogen (NOx).

-

Annual tailpipe CO2 emissions: This helps you compare a vehicle's contribution to greenhouse gas emissions over a given distance.

Using this guide can inform you as to not only how much carbon dioxide each vehicle emits, but how expensive it is to run and how much it contributes to urban air pollution.

Best performing green cars

According to the Green Vehicle Guide, Australia has 13 car models that emit zero CO2 per kilometre:

|

Rank |

Make |

Driveaway price |

Fuel type |

CO2 (g/km) (Best Variant) |

|

|

1 |

Hyundai Ioniq |

$35,140-$53,010 |

Electric |

0 |

|

|

2 |

Hyundai Kona |

$24,300-$65,290 |

Electric |

0 |

|

|

3 |

Renault ZOE |

$49,490 |

Electric |

0 |

|

|

4 |

BMW i3 |

$68,700-$70,900 |

Electric |

0 |

|

|

5 |

Renault Kangoo ZE |

$49,990 |

Electric |

0 |

|

|

6 |

Tesla Model S |

$124,900-$152,218 |

Electric |

0 |

|

|

7 |

Nissan Leaf |

$49,990 |

Electric |

0 |

|

|

8 |

Tesla Model 3 |

$67,900-$94,901 |

Electric |

0 |

|

|

9 |

Tesla Model X |

$133,900-$176,918 |

Electric |

0 |

|

|

10 |

Mercedes-Benz EQC |

$137,900-$145,600 |

Electric |

0 |

|

|

11 |

Audi e-tron |

$137,700-$159,600 |

Electric |

0 |

|

|

12 |

Jaguar I-Pace |

$123,488-$151,448 |

Electric |

0 |

|

|

13 |

Porsche Taycan |

$191,000 |

Electric |

0 |

|

Source: Green Vehicle Guide as of September 2020. Cost data via Carsguide.com.au.

As you can see, price can be quite a barrier to buy some of these cars (more on this later), but affordable electric options include the Hyundai Ioniq and the Hyundai Kona. The remainder of the top 20 includes plug-in hybrid cars such as the Mitsubishi Outlander PHEV (43 CO2 g/km), and the Volvo S60 (46 CO2g/km).

Green car loans can provide a discount

'If every new car buyer chose the lowest emissions car available, our national average carbon emissions would improve by 50%.' – National Transport Commission.

A handful of lenders offering car loans also provide a special ‘green car discount’ of their standard car loan interest rates for cars that meet their eligibility criteria. These interest rate discounts vary between lenders, but are generally around 50-100 basis points (0.50% p.a - 1.00% p.a), meaning some green car loan rates are among the cheapest on the market. They might also waive certain fees, like the Bank Australia loan which waives the $150 establishment fee.

These loans are usually offered in partnership with the CEFC to assist banks in taking on more low-emissions technologies.

How do lenders determine which cars get a green discount?

Despite what the name might tell you, your car doesn’t technically need to be green or electric to qualify for a green car loan. In fact, there are some diesel cars that can qualify for one.

As long as you meet the usual car loan criteria, the standards for getting a green car loan can include the following:

-

It is a new car model

-

It’s a hybrid or electric vehicle

-

It’s more fuel-efficient than the average car of its size

Bank First, for example, says:

"The lower interest rate is available to cars with C02 value of 180 g/km or less. Generally, this will include new cars, hybrid cars or cars that have lower emissions for their size".

You should check the Australian Government Green Vehicle Guide to see if your intended vehicle is included, remembering too that each lender will likely have a slightly different list of cars.

How green are the most popular cars?

According to the Government’s Green Vehicle Guide, the following car models are the most popular choices among Australian drivers. Here’s how environmentally friendly they are:

|

Rank |

Make |

Driveaway price |

CO2 (g/km) (Best Variant) |

|

|---|---|---|---|---|

|

1 |

Toyota RAV4 |

$31,290 - $50,275 |

107-172 |

|

|

2 |

Ford Ranger 4x4 |

$53,000 - $77,190 |

195-234 |

|

|

3 |

Toyota Hilux 4x4 |

$48,150 - $69,990 |

188-277 |

|

|

4 |

Toyota Corolla |

$23,335 - $35,645 |

81-159 |

|

|

5 |

Mazda CX-5 |

$30,880 - $52,330 |

158-174 |

|

|

6 |

Hyundai i30 |

$20,440 - $47,910 |

119-186 |

|

|

7 |

Kia Cerato |

$21,490-$33,690 |

158-174 |

|

|

8 |

Mistubishi Triton 4x4 |

$22,490 - $52,790 |

208-225 |

|

|

9 |

Toyota Prado |

$54,090 - $88,990 |

208-266 |

|

|

10 |

Mazda 3 |

$25,240 - $41,590 |

127-154 |

|

Source: Green Vehicle Guide, data sourced from VFACTS.

Most of them are below that 182 average.

[See also: Australia’s most popular car brands]

But what are the most popular green cars?

Based on our own analysis of Federal Chamber of Automotive Industries (FCAI) data, the following are the most popular cars throughout the whole of 2019 that would likely qualify for a green car loan, based each model’s combined carbon emissions.

-

The Ford Ranger

-

Toyota Corolla

-

Hyundai i30

-

Mitsubishi Outlander

-

Toyota Camry

-

Subaru Forester

-

Mazda CX-3

-

Volkswagen Golf

You’ll notice some of these cars (highlighted in bold) feature in the list of 10 most popular cars. So if you’re thinking of replacing a gas guzzler with a more carbon-friendly model, you’d be hard-pressed to go wrong with some of these options, which as you can see in the table above, can be much more affordable than their fully electric counterparts for the time being.

Will green cars become the norm?

Electric vehicle adoption might be gathering pace in Australia at the moment, but it’s still fairly slow. On a yearly basis, hybrid sales were up 111.8% in October 2020, while electric vehicle sales grew by 14.1%. According to the ABS, they still only account for around 0.1% of the national fleet.

That could be set to change, however. RenewEconomy (a news site on Australia’s climate and energy) rather boldly predicts there will be no new petrol cars sold in Australia by 2027, while the CSIRO perhaps more reasonably predicts full electrification of electric vehicles within the next 30 years. This is more in line with emissions targets set by various states like the ACT, which plans to phase out fossil fuels by 2045. Internationally, countries like the UK have ambitious targets, with Prime Minister Boris Johnson promising to ban the sale of diesel and petrol cars by 2030.

That’s not to say electric and hybrid cars are perfect, nor will the transition be easy. It’ll still cost billions of dollars of government investment, while consumers still remain hesitant to buy electric vehicles due to:

-

The upfront cost of buying one (more on this further down)

-

‘Range anxiety’ that is, the worry over relatively low distances achieved on a single charge

-

A lack of charging stations and EV infrastructure

-

A lack of model choice, as there are still few electric options available.

According to RACQ Head of Public Policy Dr Rebecca Michael, these problems should be solved with proper government investment and with more electric vehicle options entering the market.

“Over time we are seeing these becoming less of an issue, with more vehicle options coming to market in Australia, chargers becoming faster and more powerful, and better access to electric vehicle chargers across the major roads around Australia,” Dr Michael told Savings.com.au.

“Studies have also shown that most EV owners choose to charge their vehicles at home, and once familiar with the process of charging, have much less concern about their range and recharge time.”

Is enough being done to stimulate green car adoption?

Dr Michael says Australia still lags behind many other developed countries in the uptake of 'sustainable' car models like electric and hybrid cars.

“This is partially due to a lack of policy support and incentives for these new vehicle technologies. Countries where uptake is highest are generally associated with some form of government incentive or rebate,” Dr Michael said.

“Additionally, many other international governments encourage manufacturers to supply a greater range of fuel-efficient vehicles to the market by imposing stricter fuel quality standards and emissions targets.”

Australia doesn’t have anything like this on a Federal level, with the closest thing to an incentive being a higher threshold for the luxury car tax (LCT), which some experts argue shouldn’t be a thing at all, as well as a lack of a fuel-excise. Other than that, Australia mostly has state-based incentives for wannabe electric and hybrid car owners:

-

The Australian Capital Territory waives stamp duty and gives free registration for electric cars, and also offers interest-free loans up to $15,000

-

Victoria exempts electric cars from the “luxury vehicle” rate of stamp duty and offers a $100 yearly discount on registration.

-

Queensland charges a lower rate of stamp duty of 2% on purchases (RACQ is lobbying the government to eliminate stamp duty on all new cars and to reduce registration costs by 30% for low emission cars)

-

And NSW offers a small discount on registration costs

The other states (South Australia, Western Australia, the Northern Territory, and Tasmania) currently don’t offer any incentives.

[See also: Car stamp duty by state]

More broadly, an FCAI spokesperson told Savings.com.au in November that the lack of government incentives is hamstringing electric vehicle adoption.

"EVs do remain more expensive, too, and the lack of government incentivisation – which can take various non-financial forms as well as financial – and the lack of infrastructure can impact on their appeal to the new alternative drive train consumer," they said.

Can you save money with a green car?

It is possible to save money with an electric or hybrid model: It’ll just depend on which one you get, how often you use it, and it will also require some long-term thinking from you.

The main argument for owning an electric car is that they’re cheaper to run. According to the NSW Government, they’re much cheaper to run and maintain than petrol vehicles, providing savings up to 70% on fuel and 40% on maintenance costs.

“A typical car travelling 13,700 km a year would save an average of $1000 (or $1200 if the vehicle charges overnight on an off-peak electricity tariff rate),” Transport NSW said.

Overall, separate research from RACQ (seen in the infographic below) shows electric vehicles are cheaper to run than larger cars but are still slightly above the average car ownership cost ($1,273 vs $1,156 per year) in 2020 after factoring in fuel, depreciation, loan repayments, maintenance and registration.

Electric cars sometimes depreciate slower (a Tesla Model S holds 82.5% of its value after three years) and cost less in terms of fuel, but can be much costlier to maintain, and based on their high upfront costs, can have much higher loan repayments.

But one of the main factors holding back electric car uptake, aside from a lack of choices, is the higher upfront prices. While there are some affordable models, the GVG tables further up in this article shows most electric cars at the moment, such as Tesla models, can easily cost in excess of $100,000, with some getting even closer to $200,000.

Savings.com.au crunched the numbers in June, and found some hybrid or green cars could take upwards of ten years to recoup the extra costs compared to their non-green counterparts.

“While electric vehicles will generally have lower maintenance and operational costs, full electric vehicles still have a significantly higher upfront cost of purchase and therefore loan repayments compared to their Internal Combustion Engine (ICE) counterparts,” Dr Michael said.

“This high purchase price, unfortunately, offsets a lot of the savings from lower running costs.

“However, many hybrid models are much closer in price point to their regular petrol/diesel counterparts and this smaller difference can be offset by savings in fuel efficiency, likely saving their owners money in the long run.”

According to Dr Michael, many industry experts expect electric vehicles to reach price parity with ICE models in four to five years.

“Currently, the battery cost makes up a significant part of the overall cost of the vehicle, but EV purchase prices will continue to fall as battery costs reduce in coming years,” she said.

“As more models are added to the market and the second-hand market increases, competition will grow and sale prices will come down.”

The pros and cons of green cars

|

Buying a green car: Pros |

Buying a green car: Cons |

|---|---|

|

If you’re concerned about the climate, a green car is one of the biggest ways to reduce your carbon footprint. |

They still represent a small portion of the market, and there aren’t many models to choose from at the moment. |

|

As the industry continues to grow, you could get government subsidies to buy one. |

So far there has been a lack of federal action on this front - subsidies will depend on your state for the time being. |

|

Certain models can have cheaper running costs. |

They can also be more expensive to maintain. |

|

Some green cars are also quite affordable. |

The ‘affordable' electric cars don’t always look that nice. |

|

Good EV models can drive long distances on a single charge. |

Charging infrastructure at the moment is still fairly limited, and some do have short ranges. |

|

You can get substantial home loan discounts with a green car. |

A higher upfront cost could negate this discount through larger repayments. |

|

They cause less noise pollution (i.e they’re quieter). |

If you aren’t ready to take the plunge to fully electric cars yet, hybrid models use both electric and combustion engines (petrol) to give you the best of both worlds.

Savings.com.au’s two cents

‘Green cars' in terms of car loans don’t necessarily have to be electric or hybrid cars: They just simply have to be more fuel-efficient than the average car of their size in most cases, and if you meet the criteria, then you could save yourself hundreds off your car loan repayments.

However, if you aren’t satisfied with meeting some arbitrary criteria, then going full electric is a possibility. These cars are still a rarity in Australia - upfront costs, a lack of infrastructure and incentives, and a lack of choice - currently make it harder to break into the EV market. Some of the top range models like the Teslas are very expensive. The Model S starts at nearly $150,000, while Tesla’s ‘entry-level’ model, the Model 3, starts at around $70,000. If you can afford one of those then go for it, but be aware you could miss out on some of those ongoing savings for a while.

On the other hand, some of the cheaper EV models like the Hyundai IONIQ or the Nissan Leaf will usually set you back around $50,000 before on-road costs. If you can get a used one then you could end up paying even less.

Video source: Performance Drive

Over time, electric cars should become easier and less expensive to buy and maintain, and when more government investment arrives, that could be a good time to buy-in. Until then, there’s no pressure to buy an electric vehicle because you feel you have to: Compare a good number of cars and car loans to find one that suits your budget and driving needs. Remember there are plenty of non-hybrid and electric cars that produce low emissions as well, so use the Green Vehicle Guide (GVG) to find one, and make sure you compare low rate car loans with Savings.com.au.

Photo by Ralph Hutter on Unsplash

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Alex Brewster

Alex Brewster

Brooke Cooper

Brooke Cooper