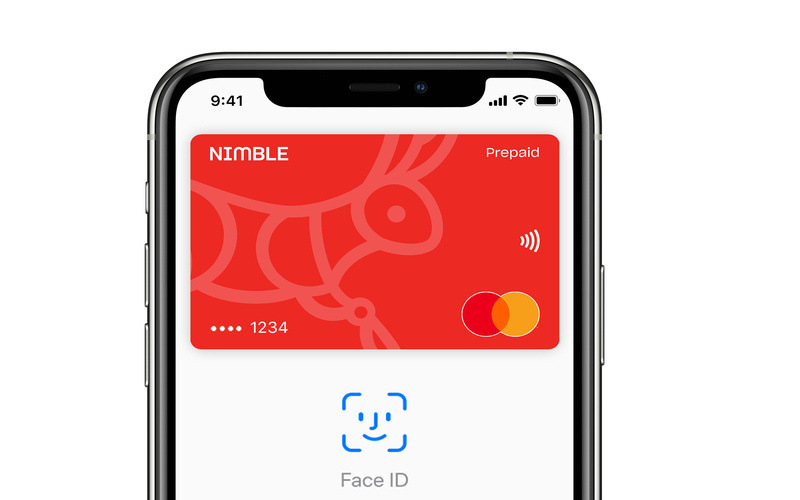

Nimble AnyTime is a virtual Mastercard, available on digital wallets like Apple Pay and Google Pay, providing customers with a line of credit between $1,000 and $10,000.

The product is designed to help customers with 'mindful spending', following Nimble's research finding one in four (27%) Aussies cannot pay an unexpected bill of $1,000.

That figure rises to one in three (33%) for 18-24-year-olds and 30% for 25-34-year-olds, while one in three Australians (34%) do not have an emergency fund for a rainy day.

Commenting on the launch, Nimble CEO and Managing Director Gavin Slater said these stats were proof of the need for change.

"Through the launch of Nimble AnyTime we’re doing exactly that; catering directly to a growing market and the evolving needs of Australian consumers today," he said.

“Too many Australians still suffer from financial exclusion by mainstream banks; excluded because they don’t qualify within narrow, inflexible lending ‘profiles’.

"This is more than just the launch of Nimble AnyTime Virtual Mastercard, it’s the latest move in our commitment to responsible lending and exiting the payday lending sector - a transition we expect to complete in 2022."

Nimble CEO Gavin Slater. Photo supplied.

As a payday lender, Nimble has attracted its fair share of scrutiny: In 2016 it was ordered by ASIC to refund more than $1.5 million to over 7,000 customers after ASIC found it had failed in its responsible lending obligations.

“Nimble failed to make proper inquiries of consumers’ requirements and objectives, and inquiries that were made were of a general nature and resulted in not enough information for Nimble to fully understand the consumers' needs,” the regulator said at the time.

After former NAB Executive Slater took over in 2018, Nimble quickly announced intentions to become a digital bank and exit payday lending, while still intending to offer short-term credit to those who need it.

Now, Nimble AnyTime has been launched to "cater to the growing market of Australians seeking a more responsible alternative to BNPL solutions."

"We take seriously our responsible lending obligations and only lend to customers who we’ve determined can comfortably make their loan repayments," Mr Slater said.

"Through Nimble AnyTime, we’re continuing to deliver on our mission to make essential financial products and services - at fair and flexible rates - accessible to millions of Aussies.”

But just how fair and flexible is Nimble AnyTime, and does it walk the talk of offering affordable credit responsibly?

The table below features personal loans with some of the lowest interest rates on the market.

Nimble AnyTime: rates and fees

According to Nimble, customers can borrow between $1,000 and $10,000, based on the amount requested and their personal information at the time of their application.

It will conduct a credit check during the application, and balances will be repaid over 12 months at most in weekly, fortnightly, or monthly instalments.

In terms of fees, Nimble AnyTime charges:

- No establishment fee

- A monthly fee of $10 for credit limits below $2,000, or $20 for more than $2,000

- A late payment fee of $10, charged after two days beyond the due date

- A variation fee (i.e. requesting an extension or change) of $50

- An overseas transaction fee of 2.99% of the transaction

- A duplicate document fee of $5 (optional)

For the interest rate, Nimble charges between 15.99% p.a. to 25.99% p.a on the amount borrowed, prior to any of the above fees.

Nimble AnyTime vs credit cards

Based on these fees and interest rates, Nimble AnyTime can come out looking worse compared to most buy now, pay later platforms (BNPL) and some credit cards.

Credit cards charge an average interest rate of 17% p.a, according to Commsec, but offer as many as 60 or more interest-free days, meaning interest is not always charged on the whole amount.

Credit cards also charge annual fees that can be anywhere between $20 and $750, with the higher fee cards generally offering extra perks and features.

Similar fees charged by credit cards include:

- Late payment fees up to $35

- Overseas transaction fees between 1% and 4%

Not all credit cards charge these fees: The table below displays some credit card products that have no annual fee.

The Kogan Money

Black Card

0% p.a.

interest on Balance Transfersx for 12 months

Product Features

- No Annual Fee

- Bonus $300 Kogan.com Credit†

- Complimentary Kogan First Membership‡

Earn uncapped rewards points!#

Product Features

- No Annual Fee

- Bonus $300 Kogan.com Credit†

- Complimentary Kogan FIRST Membership‡

xReverts to cash advance rate. Credit criteria and T&Cs apply

"Unlike a credit card, [Nimble AnyTime] repayments are linked to the limit rather than the balance," Mr Slater told Savings.com.au.

"Instead of repaying the credit card debt over multiple years, AnyTime is paid back in full within 12 months of each purchase, in either weekly, fortnightly or monthly instalments - whichever best suits their financial situation.

"And the best thing, there are no fees for paying off the loan early.”

Nimble AnyTime vs buy now, pay later

BNPL products like Afterpay can be cheaper than credit cards (research shows credit cards can charge 7x more in fees compared to Afterpay).

Most of these platforms don't charge any interest, with the few exceptions being for larger purchases.

In fact, most BNPL providers also don't charge fees unless the user misses a repayment: Afterpay for example charges $10 for not meeting a repayment by the due date, and another $7 for any subsequent missed repayments.

$10 is usually the maximum for single late fees, and as Savings.com.au broke down, only a handful of these products charge monthly account fees, like Humm.

"BNPL services can be a good option for some people as the offering is easy to access, but it encourages ‘wants-based’ shopping rather than ‘needs-based’, mindful spending," Mr Slater said.

“Without a comprehensive credit check or a meaningful assessment of a customer's ability to repay the full amount, BNPL services can see some users get into financial difficulty. We take seriously our responsible lending obligations and only lend to those who we’ve determined can comfortably make their repayments.

“BNPL repayments are often linked to transactions rather than a total balance, so customers can be faced with multiple payments on multiple dates across a fortnight which is difficult to budget and plan for."

Related: Does buy now, pay later affect your credit score?

So is Nimble AnyTime worth using?

By borrowing $2,000 with Nimble AnyTime with the 'good' credit rating interest rate of 19.99% p.a and monthly repayments for 12 months, a customer could expect to pay fixed repayments of $195.43 a month, or $2,345 in total.

Credit cards can be more expensive at times. By using ASIC's credit card calculator, making only the minimum repayments on a 17% p.a credit card for $2,000 would take 16 years to pay off at a cost of $5,067.

But by paying off that $2,000 purchase straight away, there would be no extra cost bar the annual fee, and by making higher repayments (say $100 a month), the total cost would be $2,329.

Related: Payday loans vs personal loans

According to Mr Slater, Nimble AnyTime can be worth using compared to credit cards and BNPL as it is a more responsible product.

“If we don’t believe they (the customer) can comfortably repay their loan, we don’t offer it to them in the first place,” he said.

“What’s important to remember is that because the Nimble AnyTime debt will be paid back in full in 12 months, the actual cost of the interest is much lower than many other loans; the effective rate charged is in line with the actual costs of a traditional credit card when fixed fees, such as annual fees, are taken into account.

As Nimble transitions towards being a bank, the interest rates on its loans will be lower.

“Once we have achieved the right level of scale and capital base, we will then revisit the process for applying for a banking license. It takes time, and we want to do it the right way, not the fast way,” Mr Slater said.

“The interest rates we charge are linked to our own cost of borrowing the money, and as we transition the business, we'll be able to charge our customers less.”

Be wary of high-cost loans for borrowing

Nimble AnyTime is regulated as a type of credit card under Australia's responsible lending laws, which according to Financial Counselling Australia CEO Fiona Guthrie is a vital consumer protection.

But Ms Guthrie told Savings.com.au this product still looks like a very expensive option.

"The APR may range from 15.99%-25%, but there are also account keeping fees. By the time you add these in, the actual cost of the product will be quite expensive," Ms Guthrie said.

"One of the problems across the credit market at the moment is that with these new forms of ‘credit cards’ with their various combinations of interest rates and account keeping fees, it is really hard for people to know their true cost.

"This makes it harder to shop around."

Ms Guthrie also said it was always concerning when people need to borrow for everyday goods and living expenses, which AnyTime seems to be made for.

"This usually means that there are more fundamental financial issues. Going into debt is likely to make things worse," she said.

"More debt means that you reduce your future disposable income, and that risks a debt cycle.

"It is always worth reminding people that if they’re having trouble making ends meet, that free and confidential help is available by ringing the National Debt Helpline on 1800 007 007 to talk to a financial counsellor."

Photo via Nimble

Harry O'Sullivan

Harry O'Sullivan

Brooke Cooper

Brooke Cooper

Aaron Bell

Aaron Bell

Harrison Astbury

Harrison Astbury